The ASX200 again surrendered early gains on Tuesday and we ended the day down 0.6% with around 65% of stocks closing in negative territory, not a good Melbourne Cup for Australian equities. The value stocks were the standout losers as the market continued to worry about rising interest rates stifling global growth i.e. Financials -1.3%, Energy -1.1% & Materials -2.1%. China also continues to pressure the influential Australian iron ore and coal names but with panic comes both market tops and bottoms and as subscribers know we feel these respective sectors are in / approaching buy territory, albeit for the “Active Investor”.

However we must acknowledge that the news out China is creating significant headwinds for these sectors and forays into the space should be regarded as fairly short-term in nature but commodities are cyclical beasts where selling strength and buying weakness often pays dividends:

- Coal has now fallen around 45% from its October high dragging the likes of Whitehaven Coal (WHC) down over 35% over the same period – currently feels the weaker of the two.

- Iron ore has been smacked over 55% from its May high, which has for example caused Fortescue (FMG) to fall over 47% – a maturing move in MM’s opinion.

We believe the relatively small losses by the iron names yesterday while the bulk commodity was plummeting illustrates perfectly a market looking for a low i.e. iron ore was limit down in Asia at one stage and ultimately it closed down almost 6% but FMG continues to hold onto the $14 area, where it’s held since late September – in our experience stocks lead and in this case we feel they’re calling a low in iron ore sooner rather than later.

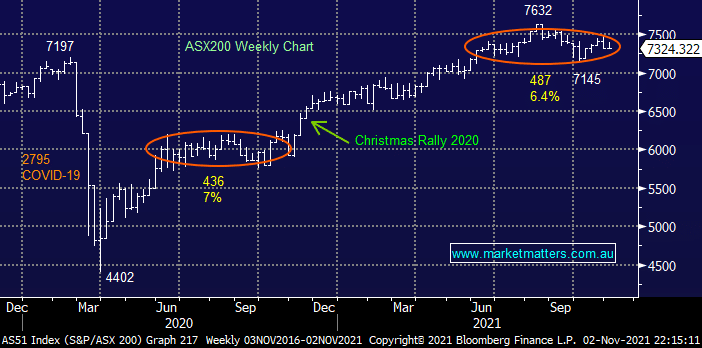

Early November is historically an average time for stocks before we start the rally into Christmas hence it should be no major surprise how the ASX has reacted to the RBA and aggressive moves by China. However bond markets saw yields drift overnight while the $A was smacked 1c back down towards 74c implying the RBA aren’t going to be forced to hike rates as aggressively as some thought earlier in the week and as our title suggests the ASX can now move on from watching the 3-year bond yield almost hour to hour.

Overnight US stocks continued to march higher with the broad market up 0.4% while the small cap Russell 2000 finally made fresh highs, the ASX200 appears set to embrace the calming of bond markets with the SPI futures pointing to a solid gain of 1% this morning which should see fresh November highs.

MM remains bullish the ASX targeting fresh highs in the weeks / months ahead

Add To Hit List