The ASX200 slipped 0.25% yesterday but considering the generally negative leads from overseas indices and sheer panic that washed through Australian interest rate markets it actually felt like a solid performance. The selling frenzy that’s washed through bonds this week feels akin to how stocks plummeted when COVID first raised its head although its coverage is primarily limited to the financial press, for now:

- The RBA is still saying no rate hikes before 2024, an outlook that MM has always thought was extremely optimistic – banks are starting to edge fixed rate mortgage higher suggesting they’re doubting Philip Lowe et al.

- The RBA tried to stem the panic last Friday but its going to take a lot more than one small flex to stop this runaway train, round 2 today perhaps?

- Markets are now pricing in a 75% chance of a hike in the next 4-months and almost 5 hikes through 2022, the later would certainly catch many new home owners off guard.

The bloodbath in bond markets has not been contained to Australia, Canada for example has just brought forward its scheduled timeframe for rate hikes – as we’ve been saying for months rates are going up and its probably going to happen faster than many are thinking. I believe the RBA will be forced to adjust their stance but after they reiterated their position into yesterday’s move I cannot see it before Christmas, perhaps they will take on the market and buy another $1bn worth of April 2024 bonds this morning, similar to last Friday.

Interestingly under the hood our market was fairly relaxed and even ambivalent to the moves in money markets, less than 60% of stocks fell and with the banks starting to enjoy a seasonal bid tone we might continue to see stock & sector rotation as opposed to any meaningful move by the ASX200. The optimists would reasonably argue that everyone, even the RBA, was expecting higher rates in the coming years and if it happens sooner rather than later its just a positive reflection of the economic recovery post COVID.

Overnight US stocks rallied to fresh all-time highs as corporate America continues to deliver on earnings cementing equities as the asset class of choice – its definitely not bonds at the moment! Last night Caterpillar (CAT US) and Ford (F US) led the line while this morning after the US closed goliaths Apple Inc (AAPL US) and Amazon.com (AMZN US) reported and fell in afterhours trade, the SPI futures are pointing to a 0.25% higher open today as we say goodbye to October.

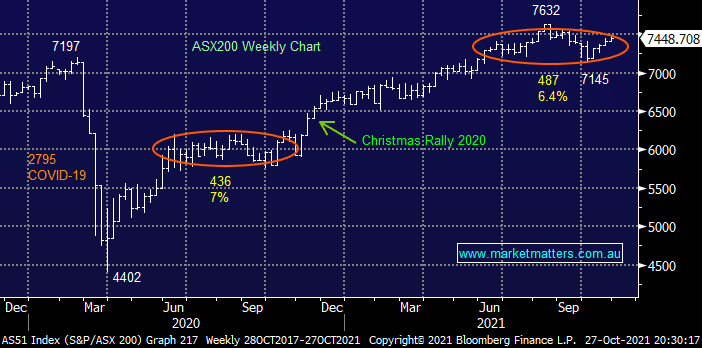

MM remains bullish the ASX targeting fresh highs in the weeks / months ahead

Add To Hit List