The ASX200 climbed to fresh October highs yesterday morning only to get clobbered at 11.30am when markets saw Australia’s inflation rate significantly surprise on the upside – the RBA’s preferred gauge, the CPI trimmed mean YoY, came in at 2.1% for the 3rd quarter compared to expectations of 1.8%, importantly the economy is rapidly approaching the RBA’s 2-3% target band for the first time since 2015 when the cash rate averaged over 2% compared to todays 0.1%.

- The RBA may still be targeting 2024 before it starts hiking rates but financial markets are thinking 2 increases before next Christmas are now the more likely path.

- As subscribers know MM believes rates are going up although the RBA can be a stubborn adversary, remember only last Friday they stepped into bond markets to “artificially” supress yields.

Nothing you haven’t heard from MM before over the last 6-months but we feel rates and inflation are going higher but I would caution that the initial “panic leg” higher in both may already be factored into some markets e.g. the $A popped to 75.36c on the inflation data but this morning most of the gains have gone. However, its been a long time since portfolios were structured for rising rates hence I don’t anticipate a flock away from value stocks but I would caution that this month’s BofA fund manager survey did show that professional investors are overweight inflationary assets such as banks and resources which probably explains the current mini-rotation back into tech.

Elsewhere on the sector level we saw the banks firm as is common this time of year, healthcare names were also strong while the iron ore names continued to weigh on the Resources Sector. The rally in Healthcare stocks caught my attention as the inflation data and subsequent higher yields and strong $A would usually act as a headwind, however the offset to this comes in the form of pricing power for the dominant ones in this respective areas.

Overnight US stocks were mixed with the tech laden NASDAQ rallying courtesy of strong reports by Microsoft (MSFT US) and Alphabet (GOOGL US) but the broader market slumped into the close, it feels tired in the face of soaring bond yields. The SPI Futures are calling the ASX200 to open down around 0.5% this morning with the resources likely to be heavy.

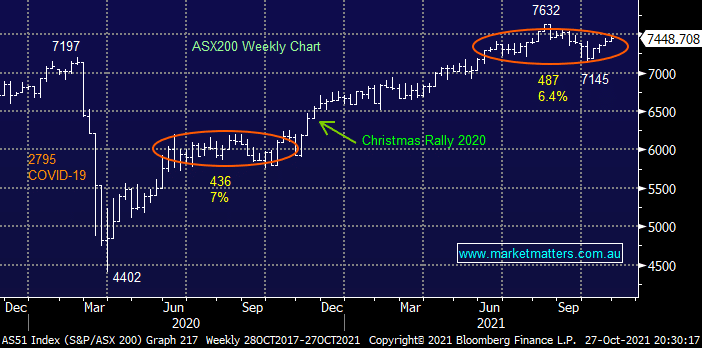

MM remains bullish the ASX targeting fresh highs in the weeks / months ahead

Add To Hit List