The ASX200 had a fairly quiet Tuesday finally closing down 0.26% in a lackluster session which saw no stocks rally, or fall by more than 5%. The Tech Sector continued to struggle even on a day when the Energy names took a well-deserved breather. Over the day US S&P500 futures appeared to direct traffic on the local market i.e. when they rallied early in the morning the ASX200 advanced around 30-points only to reverse the early gains as the US futures followed Asian indices lower after Sinic Holdings (2103 HK) became the latest Chinese real estate firm to warn of imminent default – that word contagion keeps coming to mind. Two themes continue to playout:

- Without any major external news flow Australian equities “feel” firm and well positioned to deliver a classic bullish rally into Christmas.

- However the market continues to be battered with a plethora of bad news, Sinic is a relatively new name to the China property demise but the situation doesn’t feel like it can go away anytime soon.

China’s starting to feel like Germany in World War II as they pick fights on numerous fronts, I find it amazing how many countries they appear happy to annoy (polite phrase) while at home they battle a struggling housing market and power outages that are crippling their economic recovery. Perhaps their antagonistic attitude is to create smoke screen to avoid deeper scrutiny of their own domestic issues. Beijing is likely to prop up these initial wobbles although they are major in nature, but I wouldn’t be surprised to see the worlds 2nd largest economy ultimately be the reason of the next major retracement by equities.

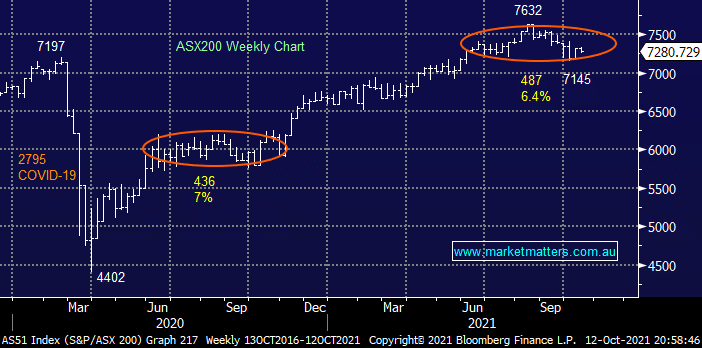

MM has maintained its bullish stance towards stocks basically since COVID raised its head and although the markets rallied over 70% we still think there’s some fuel in the tank, our preferred scenario is we see a test of the 7700-7800 area into Christmas but that’s not a huge call i.e. we’re are only looking for a rally of 6% which equates to an average gain of less than 0.5% per week.

Overnight US stocks stumbled around as trepidation set in ahead of the looming US reporting season, at least they’re not going into the important period too optimistic! Most US indices slipped around 0.3% but encouragingly the SPI is pointing to a slightly firmer opening locally, its hard to get too enthused just yet but we do like the local markets look and feel.

MM remains bullish the ASX targeting fresh highs in the weeks / months ahead

Add To Hit List