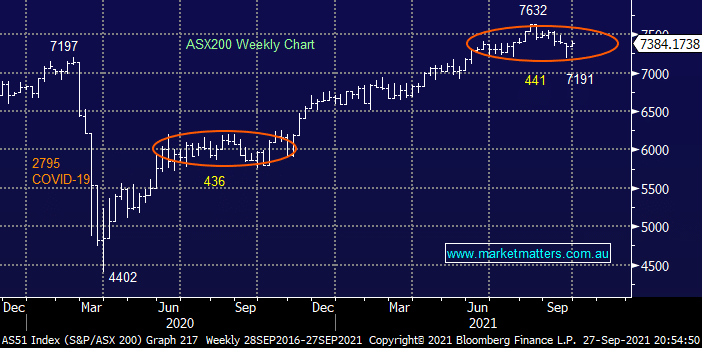

The ASX200 enjoyed a solid start to the week although it did experience some pretty aggressive selling into the close which aligns with our view that the strong post COVID rally is maturing i.e. some sellers are appearing into strength. While the banks led the charge on Monday they were very well supported by the “re-opening trade” as Gladys looks to put COVID well and truly into the rear view mirror – as she said “living with COVID won’t be easy but its manageable”. At this stage we continue to believe the markets in a similar rhythm to this time last year leading us to anticipate the following 2 scenarios:

- A few more choppy weeks around the 7400 area as different sectors take it in turns to shine feels likely.

- Eventually stocks should break out to fresh highs but MM believes this will be a move to fade / de-risk into.

The risks around China Evergrande haven’t vanished in the blink of an eye, even if Fortescue Metals (FMG) has bounced almost 15% – MM may have interest in Twiggy Forrest’s iron ore miner into fresh lows below $14. The risks and ramifications that may arise from China are very real with the next move out of Beijing being about as predictable as the weather! We do believe that eventually markets will move on and the bears will focus onto a new vein of hope but for now we foresee further relatively exaggerated swings in equities courtesy of the risks around a potential meltdown by Chinas property market.

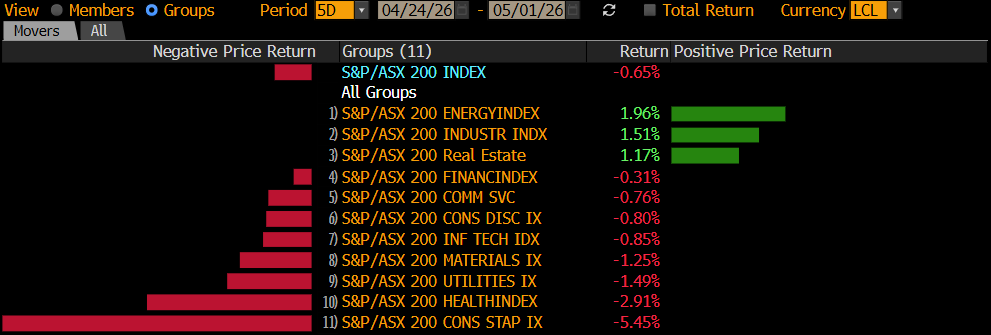

Overnight US stocks experienced a very mixed session with the value heavy Dow rallying 0.2% while the tech stocks fell 0.8%. The rotation from growth to value was triggered by ongoing strength in US bond yields which flowed through to some very different performance under the hood of the S&P500 i.e. winners Energy +3.4% & Financials +1.3% compared to losers Healthcare -1.4%, Tech -1% and Real Estate -1.2%. The SPI futures are calling the ASX200 to give back yesterdays gains this morning which feels a touch too pessimistic with the value names remaining firm.

MM remains bullish the ASX targeting fresh highs in the weeks / months ahead

Add To Hit List