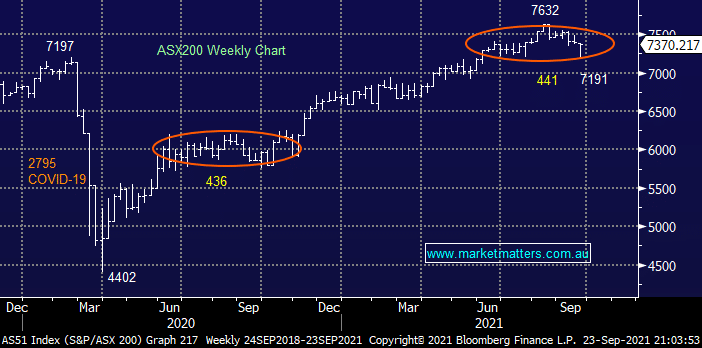

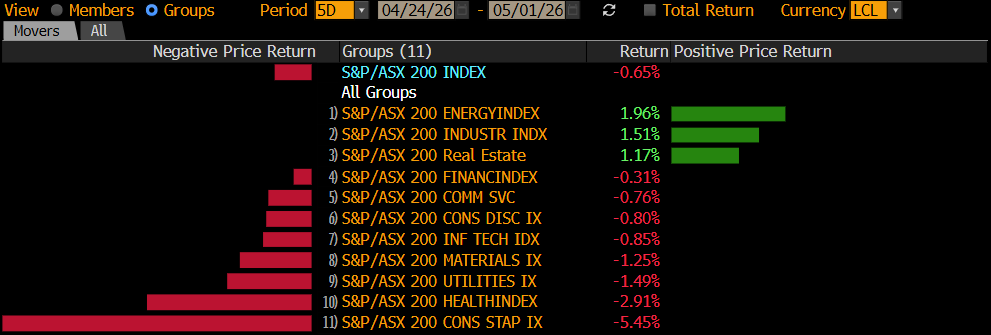

The penultimate day of the trading week saw local stocks stage a strong recovery and we commence today’s session with the index down less than 0.5% for the week, what Chinese property panic! The market enjoyed broad based buying yesterday with over 80% of stocks rallying led by the Energy and IT names although impressively all 11 sectors managed to post gains. The re-opening / economic recovery trade came back into focus as NSW’s vaccination rate continues to increase above all but the most optimistic expectations, at the current pace 90% of the eligible population will have received their first shot in just a few weeks’ time – Corporate Travel (CTD), Webjet (WEB) and Flight Centre (FLT) all rallied by over 5%.

The Feds statement after the FOMC had little discernible impact on Australian financial markets although some stability & clarity rarely hurts a stock market:

- The Fed backed the US economy to recover from COVID with tapering likely to end by mid-2022, in the process setting the stage for rate hikes later next year.

- Australian bonds paid little attention although the 3-years did nudge up slightly, “lower for longer” is still the message from local bonds.

The 1% rally by the ASX200 appeared far more correlated to a bounce in the Evergrande share price which closed up 17.6% on the day, albeit from an extremely low base. China has asked (probably told) the embattled property business to avoid a near term default on its debt, I’m sure it has a plan for the more pressing issues over the coming weeks / months, potentially some attractive pickings for state owned and private operators are looming on the horizon – one companies demise is an opportunity for another. Ironically Beijing instigated much of this mess after it tightened lending rules to rein in debt and speculation for a market that was feeling like our own but on steroids! We believe the Chinese government will maintain financial stability but the boom days feel like they are in the rear view including those for iron ore.

Overnight US stocks continued their strong ascent making it their best 48-hours since May, after digesting the FOMC meeting US 10-year bond yields rallied to their highest level in 12-weeks creating a tailwind for the resources and financials to lead the gains. The SPI futures are pointing to a marginally higher open this morning but if it gets the bit between its teeth we could easily close the week up wiping out the Evergrande mid-week losses in the process.

MM remains bullish the ASX and a keen buyer of this week’s pullback

Add To Hit List