Wednesday saw the ASX200 rally strongly from early sharp losses after the PBOC (China’s central bank) injected more Yuan than anticipated into its banking system coupled with embattled property group Evergrande announcing it would make an interest payment today – the latter is a small step along a long journey but the action out of Beijing implies the communist party intends to “manage” the situation. The market reaction wasn’t so much one of huge “risk on” as opposed to a strong bounce / sigh of relief after a tough period with the recovery most noticeable in the large cap iron ore names:

- Standout iron ore winners : Fortescue Metals (FMG) reversed 6.4% intra-day to close up 4.2% while BHP Group (BHP) and RIO Tinto (RIO) managed to bounce 3.1% and 3.9% respectively from their morning lows.

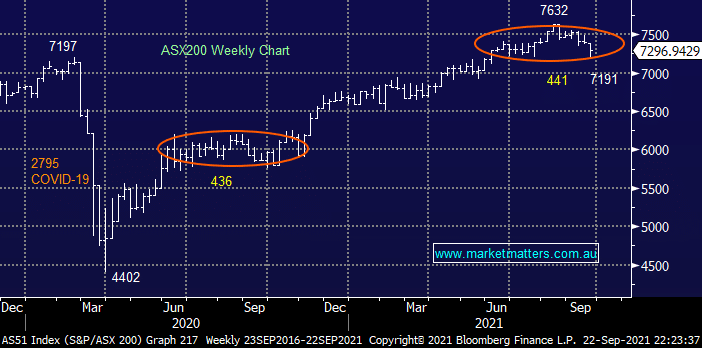

The market finally closed up a reasonable 0.3% with the Resources Sector leading the line on a day which didn’t see broad based gains, at this stage having tested our 7200 target area MM believes the ASX is “looking for a low” but its not out of the woods yet, especially as the Financials feel tired. We often say the market cannot go up without the banks and the average loss of the “Big 4” over the last 5-days is 2.9% although the insurance names are making them look good, especially after Melbourne’s scary earthquake.

This morning the Fed clarified its view towards tapering / reduction of economic stimulus with rate hikes now being priced in for 2022 after Fed Chair Jerome Powell said that tapering could end around mid-2022 implying something along the lines of an 8-month stimulus reduction process from late this year – a clear vote of confidence towards the US economy. The markets interpretation sent shorter dated bond yields up while the longer dated 10 & 30-years retreated, overall nothing scary and the market loves the removal of uncertainty.

Overnight US stocks embraced the combination of news from China and the Fed which helped US equities close up around 1% with the Financials and Energy stocks leading the line. The SPI Futures are looking for only a small gain this morning with BHPs 2% drop in the US clearly dampening sentiment – the US Materials Sector bucked the positive sentiment overnight falling almost 4%.

MM remains bullish the ASX and a keen buyer of this pullback

Add To Hit List