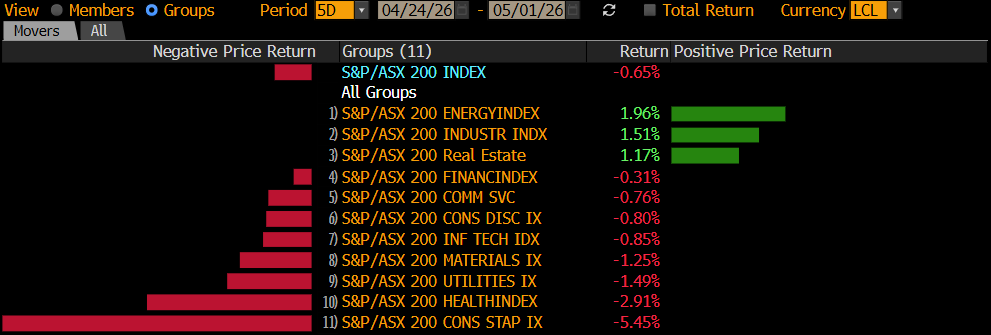

The ASX200 was hit hard on Monday falling by more than 2% on very broad based selling. The only pocket of strength coming from the utilities sector which benefited from yet more corporate activity from cashed up foreign investors, this time Canada’s Brookfield took aim at AusNet Services (AST) which is involved in electricity & gas distribution in Victoria elevating the stock by ~20%. There is certainly cash around for critical infrastructure assets that can lock in long term funding at attractive rates.

The main influence yesterday came from Asia with Hong Kong sinking over 4% during our time zone as the situation with China’s second largest property developer Evergrande spilled over into the broader market. It’s been a little over 13 years since the wall street institution Lehman Brothers collapsed under ~$US600b worth of debt and with the benefit of hindsight we can confidently say it would have been cheaper and less painful for all to bail it out instead of letting it fail. The communist government in China now have a similar decision to make, although on a smaller scale with debt of ‘only’ $US300bn. While we suspect the Government will provide a backstop it won’t be before equity investors undergo considerable pain. It’s also worth remembering that Xi Jinping has often said ‘houses are for living in, not for speculation’.

Over recent weeks MM has pushed the sector rotation button towards commodities / materials, a move that feels uncomfortable right now however it’s not a move we’re being shaken out of just yet. While it’s important to recognise that as investors we don’t get married to ideas in today’s rapidly evolving market, we have been anticipating some weakness into a seasonally weak period and for now the market is delivering on script, albeit more aggressively in some sectors than others.

A few things catching our attention as this cycle unfolds:

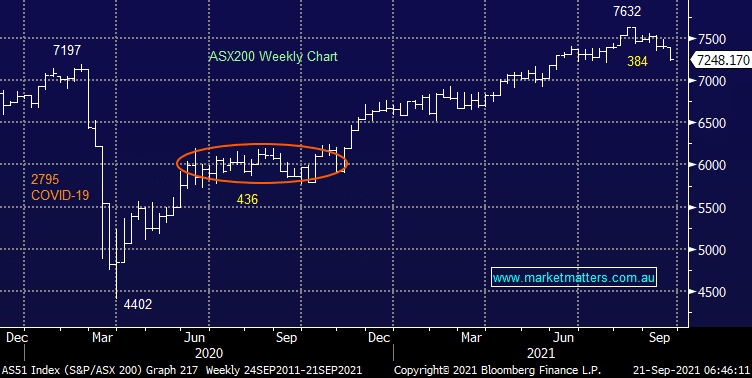

- The ASX is set to open down another ~1.3% / 100points today following a 1.8% sell-off in the US overnight. That will take the pullback for the ASX 200 to ~500 points / 6.5% from the high set a month ago.

- MM has been flagging September weakness and this pullback for now is aligned with bouts of September weakness in 2011 (-6.7%), 2014 (-5.92%), 2015 (-3.56%) & 2020 (-4.03%), noting that in most cases the market finished above the low of the month.

- We continue to believe that buying seasonal weakness in September yields strong results in the latter months of the year.

Overnight US stocks fell, bond yields ticked lower while the $US and volatility index edged higher, the S&P500 ultimately closed down 1.7% with most selling targeted to areas linked to global growth i.e. commodities while the ‘reopening trade’ such as the airlines continued to edge higher.

At 5.30am Sydney time the Dow Jones was down nearly ~1000 points however an aggressive 30mins of buying to end the day saw the Dow close 614 points lower. The SPI Futures are calling the ASX200 to open another 100-points in the red this morning, building on yesterday’s 2.1% decline. The local market will test and likely break ~7200 support this morning.

MM remains a keen buyer of pullbacks

Add To Hit List