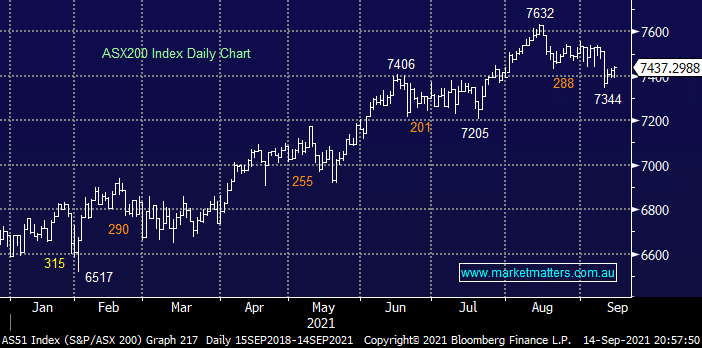

The ASX200 again recovered from early losses yesterday to close up 12-points with a 4.5% advance by the Energy Sector the clear standout, coincidentally the day after MM described it as “the cheap pocket of the market” – we remain overweight and bullish oil stocks which have fallen in 2021, even while crude oil has rallied almost 50%. The miners played a supporting role which caught our attention as iron ore plumbed multi-month lows, on balance the reflation trade is slowly gathering momentum.

The RBA is sending a slightly conflicting message in my opinion but its undoubtedly one which maintains a tailwind for equities:

- Philip Lowe et al remain optimistic towards the Australian economy believing the recent NSW & Victorian lockdowns are only a “temporary setback” to the post coronavirus economic recovery.

- However he maintains his stance / view that interest rate hikes will not occur until 2024 compared to markets which are pricing in steady rises from late 2022.

History tells us that central banks are usually too slow in raising rates and once the inflation genie is out of the bottle a painful path of aggressive rate hikes is required to curtail the runaway train. There’s obviously plenty of water to go under this bridge but overall MM believes the RBA will again be too accommodating in the next few years and markets are eventually likely to be proven correct.

However on Tuesday the reaction of financial markets to comments from the RBA Governor was to follow his lead with local bond yields and the $A falling however they weren’t dramatic moves and the next few weeks should provide a clearer picture – note as markets are pricing in hikes from late 2022 any push back from the RBA is likely to have the greatest impact on 3-year bond yields which should help keep mortgage rates down into next year.

US stocks fell overnight with all sectors closing in the red following tepid inflation data which also sent bond yields and the $US lower. The SPI futures are calling the local index to fall around 0.5% early on this morning with the resources and banks likely to surrender some of yesterdays gains.

MM remains bullish the ASX and keen buyers of pullbacks

Add To Hit List