The ASX200 enjoyed another classic 2021 day to kick off the week, it may not have managed to close on its highs but the local index still recovered from early weakness to close up 0.25%. The number of winners and losers was pretty evenly matched but the aggressive buying which rolled through much of the Resources Sector was more than enough to offset loses elsewhere e.g. OZ Minerals (OZL) +4.2% and Pilbara Minerals (PLS) +7.3%. MM remains both bullish and overweight the Resources Sector but following our purchase of Alumina (AWC) yesterday it’s probably now time to sit back and assess if we are correct, especially in our Flagship Growth Portfolio: Click here to view

In our opinion 2 factors contributed to yesterday surprising strength, remember the futures on Saturday morning were calling the ASX to open very much on the backfoot come Monday morning:

- Before the market opened we learned that Sydney Airports (SYD) was now recommending a revised $8.75 bid, third time lucky – if the ASX200’s 19th largest stock can be acquired is anyone safe?

- The US S&P500 fell 35-points on Friday but the futures market enjoyed some strength creeping back in before they took off around 3pm AEST, dragging the ASX200 up around 0.5% in its slipstream.

The last few months has seen the takeover activity / outcomes come off the boil slightly as some suitors walked from their prey including 2 of MM’s holdings – Crown Resorts (CWN) and Altium (ALU). However the increased bid for SYD, which got the boards nod for further due diligence looks to have reminded investors that the world is still awash with money plus mountains of cheap debt is readily available, we believe this market phenomenon just took a “little nap” and more bids will again start crossing our screens.

Overnight US stocks were mixed with Energy stocks best on ground as crude oil hit 6-week highs, lucky many of us are not driving anywhere at the moment! We feel traders are waiting on this weeks inflation data which could determine the path of stimulus withdrawal and interest rate hikes, not an exciting prospect for risk assets. The SPI Futures are pointing to small early losses today with no major influences from overseas.

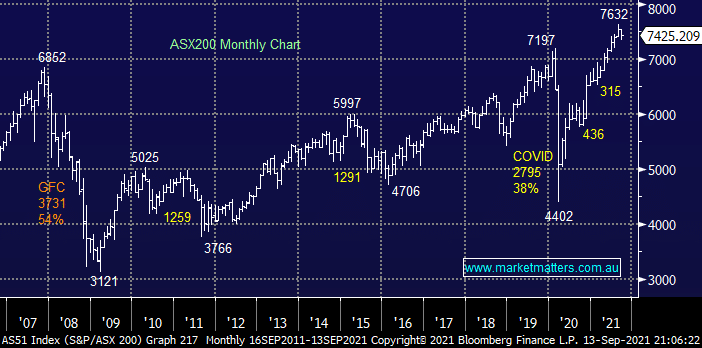

MM remains bullish the ASX and a keen buyer of this pullback

Add To Hit List