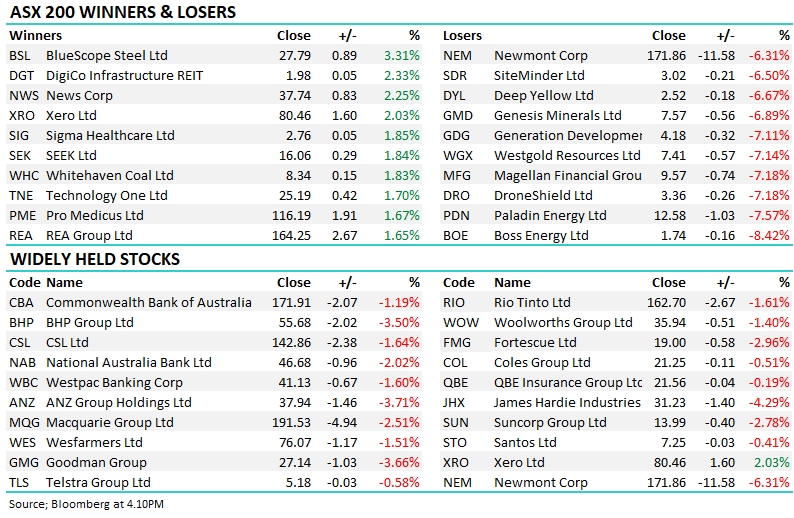

COL -7.06%: FY23 numbers out for the staples business, Coles was largely in line but it looks like it gets harder from here. Revenue of $41.5b was largely in line while EBIT at $1.97b was a small miss, driven by a softer-than-expected Supermarket result. Gross margins slipped in the second half on higher costs while CAPEX came in at the top end of guidance following delays to their new Victoria and NSW fulfillment centres. Coles has seen a slight shift away from out-of-home dining to start FY24, however, costs are up and inflation benefits are starting to subside as it moderates. Increasing wages will further impact FY24, while the company also saw higher theft levels in FY23, up ~20%, a trend that is expected to continue.

MM is neutral COL, preferring MTS in the space

Add To Hit List