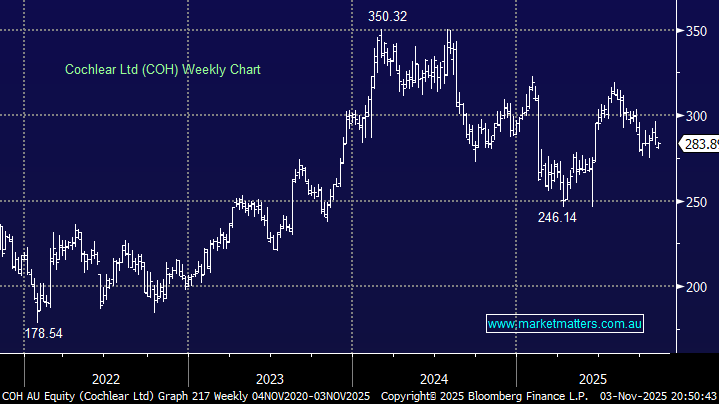

At the end of October, COH reaffirmed its FY26 earnings guidance, for an 11% to 17% increase in underlying net profit from last year. Device demand across both cochlear implants and Acoustics looks strong, while Services expectations have been reset over the last 12-18 months, which puts the stock firmly in the “buy the dip” camp for MM.

- We like COH ~$280, although it might need a fresh catalyst to push significantly above $300.

MM is bullish towards COH around $280

Add To Hit List