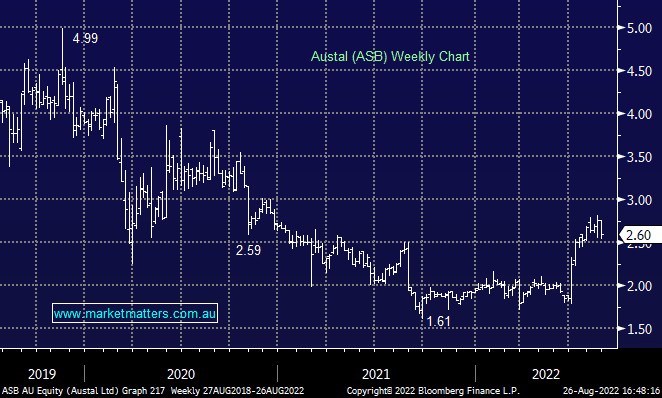

ASB -2.26%: the shipbuilder announced a good set of numbers for their FY22 result today, though it failed to ignite the stock. EBITDA was in line with pre-guided numbers at $120.7m, up 5.3% on the back of the recently awarded OPC contract that could be worth up to $3.3b in revenue. It’s positive to see the new steel shipbuilding facility being put to work and generating new business with the company noting a larger pipeline of long-term contracts they are now available to submit tenders for. The order book grew to $3b, up from $2.5b and they guided to $100m EBIT for FY23, around 10% ahead of the market, though consensus had largely remained unchanged since the announcement of recent contract wins.

MM remains bullish and long ASB in the Emerging Companies Portfolio

Add To Hit List