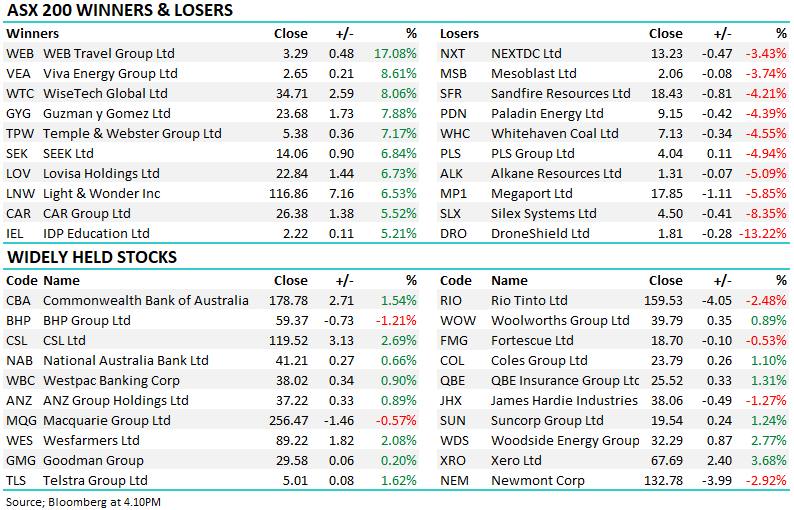

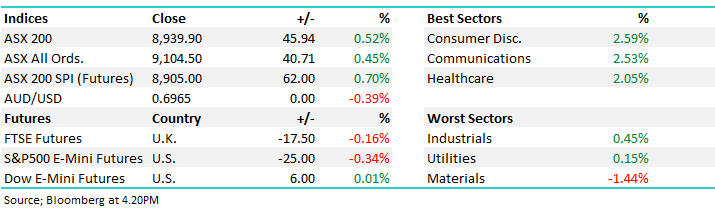

The Australian share market failed to follow the almost 5% gain by US stocks last week, primarily because the banks were soft, led by Westpac (ASX:WBC) which fell more than 7%, dragging the influential sector down 2.1%. It was one of those weeks where the bad news arrived in waves and the market had nowhere to hide even as global indices rallied around it. The ASX decline was modest until compared to its global peers.

A very weak set of Australian business and consumer confidence data set the tone early, unsurprising given ongoing cost-of-living pressures. That was followed by a fire at one of the nation’s 2 remaining oil refineries, heightening concerns around fuel security, while Westpac warned that Iran-driven interest rate volatility had hit markets income and lifted credit provisions, potentially a precursor for ANZ and NAB. Also, a strong domestic labour report reinforced expectations of another RBA rate hike in May, or June.

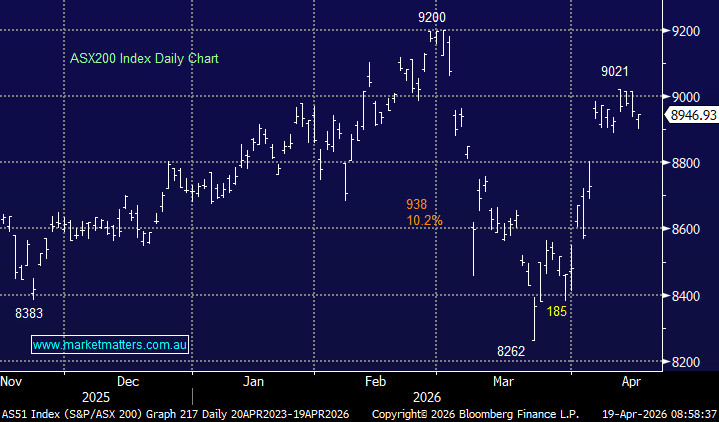

On Saturday morning, before the latest conflicting news out of the Middle East, the ASX200 was poised to open back above 9000, testing last weeks high. However, it’s a tougher call now, we would estimate a flattish open as opposed to a ~1% gain, with the AUD opening down 0.60% and Crude Oil spiking +7% higher in early Asian trade.

- No change, we continue to believe the ASX will make new highs through 2026.

MM remains bullish towards the ASX200 around 8950

Add To Hit List