I’ve noticed a number of MM subscribers are becoming increasingly nervous around the COVID outbreak in Sydney, makes sense, I know I am – this school terms basically gone and the Gerrish household is already becoming increasingly anxious around the next one! One narrative that comes to mind towards defensive investing is “we all have to eat” and with grocery prices edging ever higher across NSW supermarkets it appears profit margins for the food industry wont be squeezed by the current disruptions.

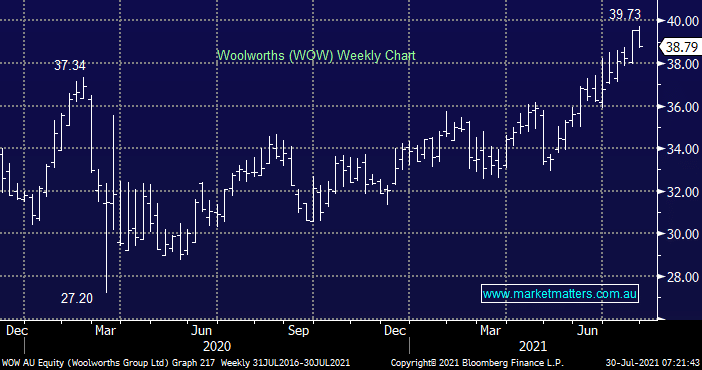

During the initial wave of COVID back in Q1 of 2020 Woolworths (WOW) experienced some wild gyrations over the ensuing weeks as investors “punted” whether lockdowns could even benefit the likes of Woollies & Coles, I understood the relative moves but ultimately families weren’t going to eat more just because they were stuck at home, with the exception perhaps of a few bags of lollies and popcorn! Hence normality quickly returned and WOW ground out gains to fresh highs basically in sync with the ASX with its valuation enjoying the tailwind of ultra-low bond yields – WOW currently yields around 2.6% fully franked.

MM feels the supermarkets will continue to move largely in line with the ASX, Metcash (MTS) our preferred sector exposure – NB we currently hold MTS in our Active Income Portfolio.

MM is neutral / positive WOW around $40

Add To Hit List