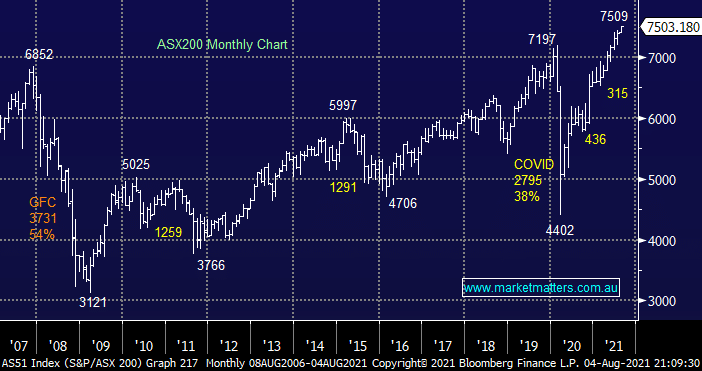

The ASX200 enjoyed a solid session on Wednesday basically closing on its all-time high, although only 55% of stocks rallied when the major banks and miners advance it’s going to be another win for the bulls. Fresh bad news is rapidly becoming increasingly thin on the ground clearing the way for further gains into Christmas for an index which has already rallied +13.9% so far this year. At MM we are bullish equities with the path of least resistance clearly to the upside, a few other additional statistics to the ones recently mentioned are also catching our attention:

- As we start a fresh month the likelihood is the ASX200 will reach the 7650 area in August, assuming the short-term 7400 support area holds firm.

- Seasonally August & September are not great for the ASX delivering an average return of -3.8% over the last decade, things usually then turn up strongly from October onwards.

- This year May & June ignored the historical statistics and obviously the next 2-months may follow suit but if we do get a decent pullback in the coming weeks MM will regard it as a prime buying opportunity.

Australian bond yields continue to drift lower while commodity prices bounce around in an uncertain manner as economists attempt to unravel how the world will recover from the Delta Strain, at MM we believe it’s best to leave the short-term noise & guesswork to the traders / analysts while we focus our attention on a couple of key opportunities that are /may be in play over the next 6-months:

- The cost of capital remains remarkably cheap with Australian 30-year bonds still only trading around 2%, when combined with plenty of excess cash ongoing strong M&A activity appears almost guaranteed.

- Commodity prices have dipped on fears of economic contraction as the virus spreads, if they take another leg to the downside MM will be an aggressive buyer of the sector

Otherwise patience is the best game in town as the market continues to grind higher with some interesting stock / sector rotation unfolding almost weekly, we will consider the occasional portfolio tweak but major moves are unlikely until we see another chapter in the evolution of equity indices.

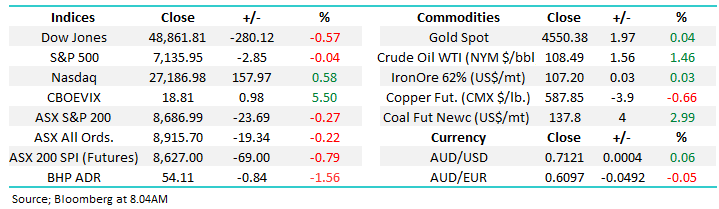

Overnight US equities had a mixed session with tech names closing marginally higher while the Dow fell over 300-points led down by the Energy Sector following oils -3.7% drop.

MM remains a buyer of weakness across most stock market sectors

Add To Hit List