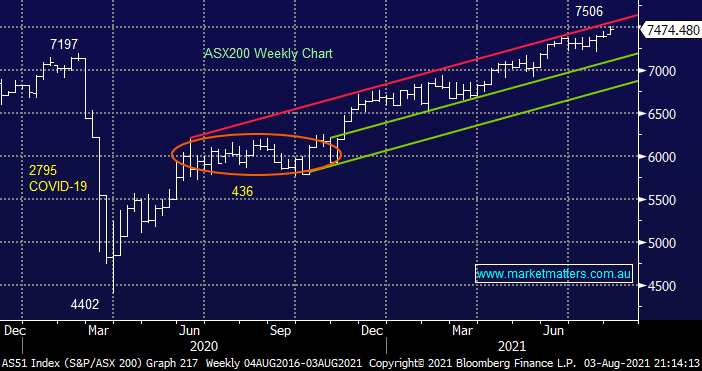

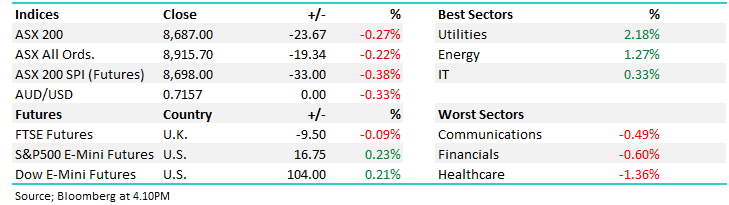

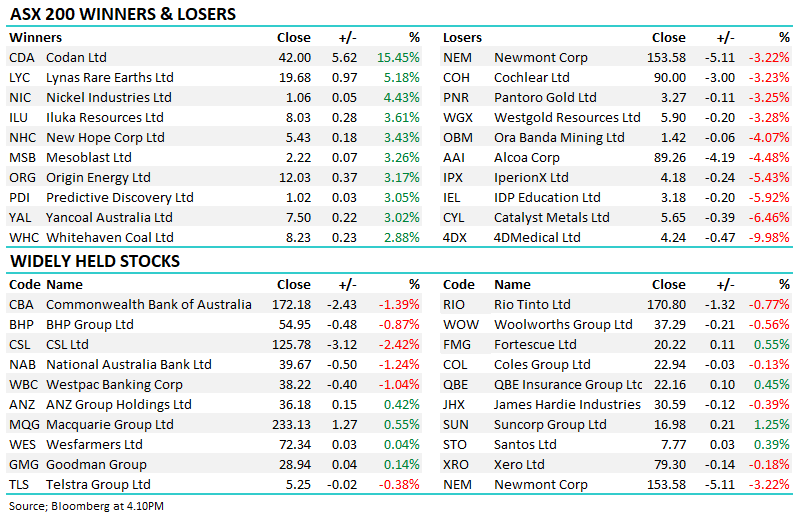

The ASX200 drifted lower yesterday although it was primarily a lacklustre session by the banks which caused the -0.2% decline. Under-the-hood the local tech space remained the hot place to be after being ignited by the $39bn takeover bid for Afterpay (APT) on Monday, the biggest corporate play in history, perhaps we’re finally going to see the local IT stocks address their major underperformance when compared to the US FANG’s & Co through 2021 – more on that later.

Interestingly on the surface Australian equities are shrugging off both good & bad domestic economic news as they focus on what comes next as opposed to the present:

- We all know that the Delta Strain is playing havoc with today’s economic stability in Sydney and now Brisbane but as vaccination rates soar investors are focusing on 2022 as opposed to the present day events.

- Yesterday saw the RBA largely ignore the recent lockdowns and signal their faith towards the resilience of the Australian economy i.e. they intend to stick to their tapering of bond purchases i.e. the first step towards higher interest rates.

Markets clearly weren’t expecting a backward step by Philip Lowe as both bond yields and the $A hardly reacted to the news, neither did equities for that matter. Financial markets are clearly anticipating solid economic expansion in 2022 with perhaps a few hiccups between now and Christmas – considering the rate of recovery since March 2020 it’s a logical outlook assuming no fresh strains catch us napping. The rhetoric from both Gladys and Scott Morrison has improved dramatically almost overnight as people step up for both the Pfizer and AstraZeneca vaccines at an ever increasing rate – my “tip” is Sydney schools will go back next term on Tuesday 5th October at the very latest.

Overnight saw US stocks rally late in the day (our morning) to close at its 42nd record close of 2021 – who says its not a bull market! Strong corporate earnings are trumping COVID fears as mask mandates are reintroduced for the likes of San Francisco. The SPI Futures are only calling the local market to open marginally higher this morning although BHP Group (BHP) rallied ~1.8% in the US overnight.

MM remains bullish the ASX and keen buyers of pullbacks

Add To Hit List