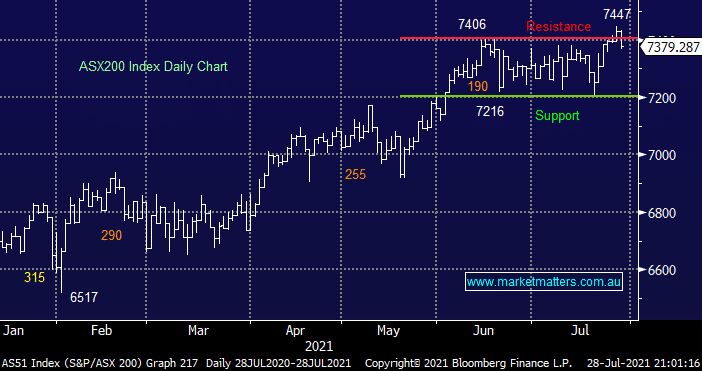

The ASX200 struggled yesterday in the face of broad based selling which ended with 70% of stocks closing lower by the end of the session. On the sector level the unusual combination of IT & Energy stocks bore the brunt of the selling although the big 3 of CBA, CSL and BHP falling an average of -1.3% had the largest impact on the underlying index. If recent history repeats itself we will be making fresh all-time highs by the start of August but Wednesdays weakness did feel like a false break above 7400, technically that would usually target a pullback towards 7200 and potentially even 7000 but this bull market has continued to quash any detractors hence MM would rather buy pullbacks as opposed to jump on board sell-offs.

A number of macro events have caught our attention over the last 24-hours although at this stage they’re generating some mixed signals:

- Australia’s inflation data came out a whisker higher than expectations although it’s now irrelevant as economists start to 2nd guess the impact of fresh lockdowns, especially in NSW – local bond yields fell to levels not seen since early February, a bearish indicator towards economic activity.

- The banks and resources struggling with declining yields is to be expected but IT carrying the wooden spoon was a surprise, unfortunately the local tech space is embracing the bad days for big US Tech but not particularly the good ones.

- Commonwealth Bank credit card data is showing a sharp down turn in consumer spending across Sydney yet most of the sector remains resolute, were not keen on the Retail Sector at present but we’ve been wrong with this one before.

- We’ve discussed the sell-off in China facing stocks this week but yesterday saw a strong ~5% recovery in related Asian indices implying it’s time for at least a rest for this negative influence from Xi Jinping et al.

Overnight we saw US stocks edge higher led by tech stocks after the Fed left interest rates unchanged and bond yields fell after Jerome Powell said “he was still a ways away” from raising rates. No S&P500 sectors managed to move by more than 1% and the Dow even fell -0.36% while the NASDAQ rallied +0.4%, the SPI futures are calling the ASX to open up ~0.2% this morning helped by more than a $1 jump in BHP Group (US) in the US.

MM remains a keen buyer of stocks into pullbacks

Add To Hit List