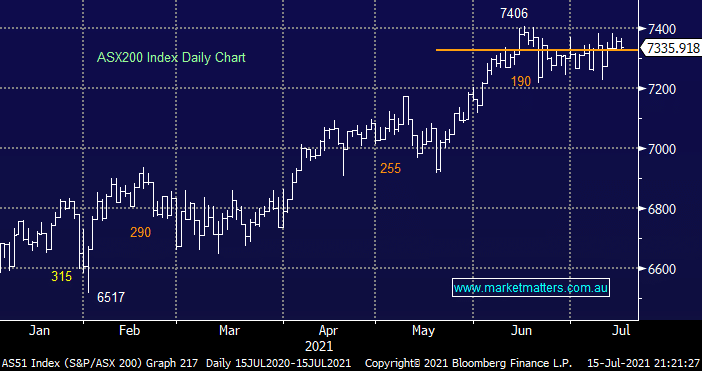

The ASX200 slipped lower yesterday, as we come into Friday “the song remains the same” with the local market very happy to simply rotate around the 7300 area whatever the macro / market news that crosses our screens. In what was a quiet session during an even quieter few weeks for stocks a few points did catch my attention:

- Some of the major banks made fresh 11-week lows which doesn’t bode well for the sector short-term, a definite headwind for the ASX.

- Spark Infrastructure (SKI) received the anticipated takeover bid at $2.80 reinforcing our view that M&A is alive and well as we enter the second half of 2022 – MM also believes there’s a very good chance of a higher bid on this one.

- The BNPL sector feels friendless and is likely to encounter selling into any bounces in the coming weeks.

- The local Tech Sector is starting to struggle even as the NASDAQ continues to rally and bond yields drift lower, a slight concern short-term.

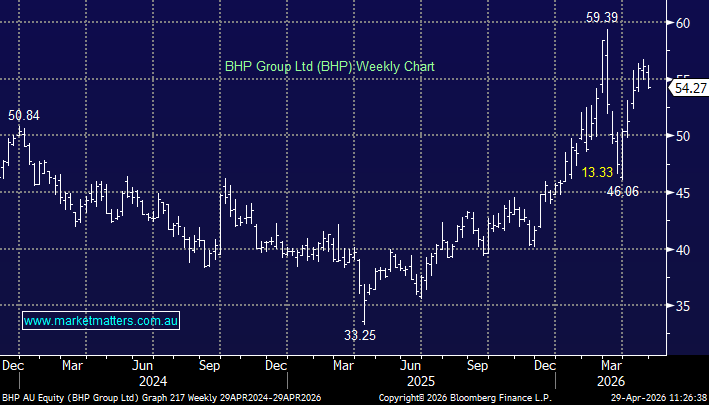

The Resources Stocks have enjoyed a strong few days since China’s PBOC announced their intention to give their economy another shot in the arm by allowing the banks greater flexibility to lend, potentially injecting over $200bn into the economy. A couple of things within this group has also caught my attention apart from the obvious strong rally by the likes of BHP Group (BHP):

- Gold stocks are really embracing the precious metals bounce from $US1,800 – it feels to us like some short-term players have been caught too bearish here.

- Whitehaven Coal (WHC) continues to rally posing the question when will the Oil Sector finally regain its mojo?

Overnight US stocks were again quiet although we saw some index reversion with the NASDAQ slipping -0.7% while the Dow edged higher. Fed Chair Jerome Powell again reiterated that its too early to scale back monetary stimulus and some concerns are percolating through markets that we may have reached peak growth, these murmurings are being reflected in bond markets but not equities. The SPI Futures are calling the local market to open unchanged this morning.

MM remains a keen buyer of stocks into decent pullbacks

Add To Hit List