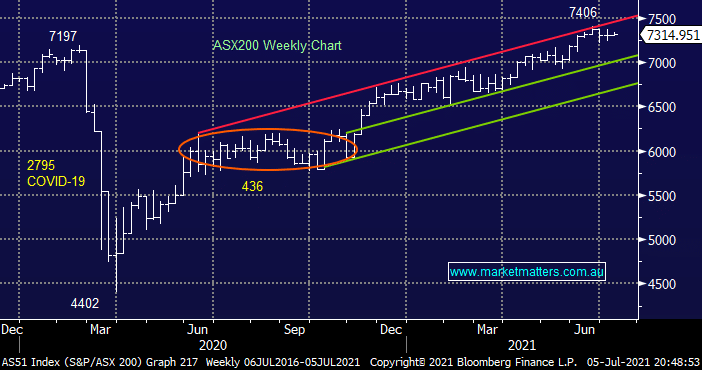

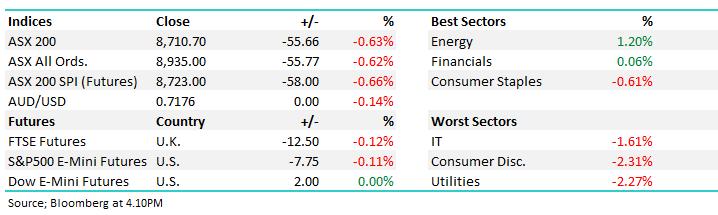

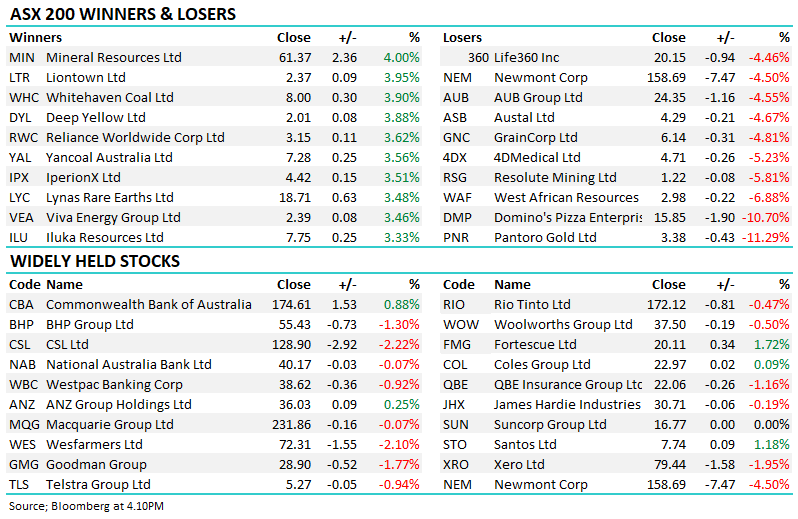

Monday morning should have reminded us all that M&A is alive and well in 2021 as an infrastructure consortium bid $22.6bn for the embattled Sydney Airports (SYD), the 42% premium to Fridays close would have sent a sigh of relief through much of the local investment community who have been major supporters of this classic “yield play” stock since the GFC. The bid not surprisingly helped the Transport Sector outperform but broad weakness in the Banking, Financials, Retail, IT and Healthcare Sectors put a dampener on proceedings with the ASX finally closing up just 6-points, we would actually have closed in the red if it hadn’t been for the +19-point positive contribution by SYD.

Overall its not surprising that we’ve experienced a lacklustre start to the week with the much awaited news on local interest rates due at 2.30pm today, the focus clearly being on bond buying / quantitative easing rather than rates themselves with any deviation from the expected path likely to have ramifications under the hood e.g. in general terms:

- Hawkish (less quantitative easing and a more aggressive path of rate hikes) – good for the $A and banks but bearish for bonds and tech / yield play names.

- Dovish (a less aggressive reduction in quantitative easing and path of rate hikes) – good for tech / yield play names but bearish for the $A / banks.

The RBA will take centre stage today especially as speculation is mounting that their message / rhetoric is set to change in line with our strengthening economy and housing market, there are plenty of moving parts to this equation:

- The easy part is official interest rates are very likely to remain at 0.1% until well into 2022.

- Expectations are for the RBA to “taper” its bond buying program but how / & by what degree is key.

- Also will they start to push back their 3-year bond 0.1% target from April 2024 to November 2025, this would reduce the current increasing pressure on home loan rates.

- Governor Philip Lowe is likely to give some insightful clues to anticipated movements by the Australian Central Bank in his media conference after the meeting in an obvious effort to convey the correct message.

We’re a bit on the fence as to today’s meeting however we continue to believe interest rates and inflation go higher with the timing the main variable. As we often say don’t fight the tape so today will not just be about what Philip Lowe says but also how the market interprets his comments moving forward.

Overnight US stocks were closed for Independence Day while European bourses drifted higher in the face of no major influences, the SPI Futures are pointing to an open up +0.2% this morning by the ASX but the RBA is likely to move the dial one way or another this afternoon.

MM remains a very keen buyer of stocks into pullbacks

Add To Hit List