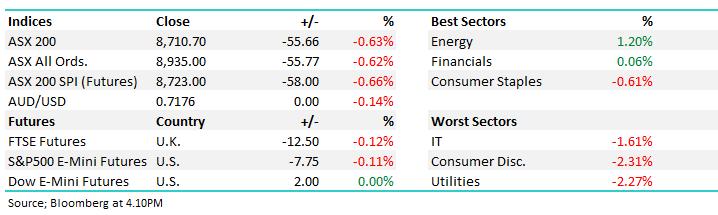

It already feels like a long week and its only Friday morning, the combination of being in lockdown and EOFY has been exhausting, the market itself is only down -0.6% so it’s certainly not any wild gyrations in stocks draining our energy levels. The delta strain outbreak still appears to be on a knife edge leaving many of us in Sydney wasting enormous emotional energy listening to Gladys at 11am each day, the very real risk of schools not re-opening in 10-days’ time has my wife Alice very much on edge!

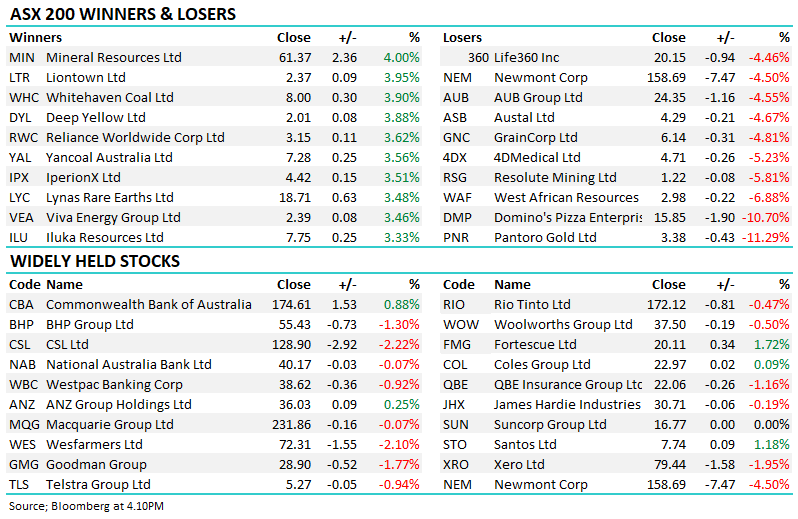

Less than 30% of stocks advanced yesterday and the number would have been much lower if the gold sector hadn’t enjoyed a solid bounce. Fund mangers are likely to complete their portfolio adjustments over the following weeks to compliment the ones into EOFY, the next performance rule off for many is on December 31st . We believe stocks will experience an ever increasing bumpy road into 2022, and beyond, but the underlying trend should remain strong for the ASX. Until further notice we are going to use the $US to benchmark our macro view which at this stage is pointing to ongoing strength in the greenback and subsequent outperformance by growth over value stocks i.e. tech continues to outperform banks & resources.

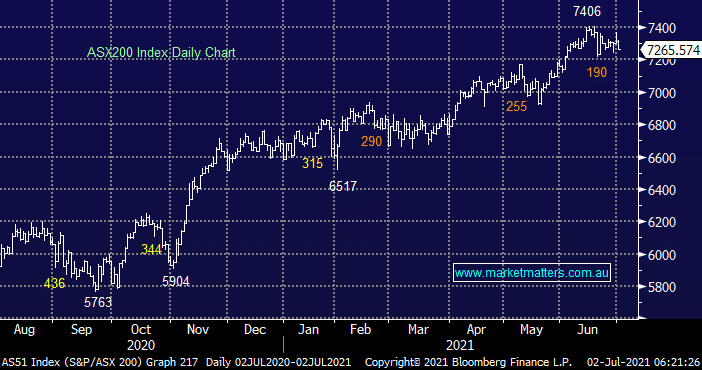

The stock market remains extremely resilient to the prospect of ongoing COVID economic disruption, the ASX200 is less than 2% below its all-time high even as the banks / resources wobble. My “Gut Feel” is the market is close to a reasonable pullback now EOFY is behind us but we remain keen buyers around the 7000 area i.e. a retracement of similar magnitude to the one this time last year. Interestingly we led the US through both consolidation and breakout phases in Q3 of 2020, perhaps 2021 will follow a similar pattern.

Overnight US stocks were firm with the Dow rallying +0.4% as it strives to make fresh all-time highs, the SPI futures are calling the ASX to open up around +0.4% this morning but it feels like a quiet day is likely.

MM remains a very keen buyer of stocks into pullbacks

Add To Hit List