Hi John,

Two very beaten-up stocks here, so a degree of trepidation is required in a market that’s more comfortable buying “certainty” as opposed to turnaround stories:

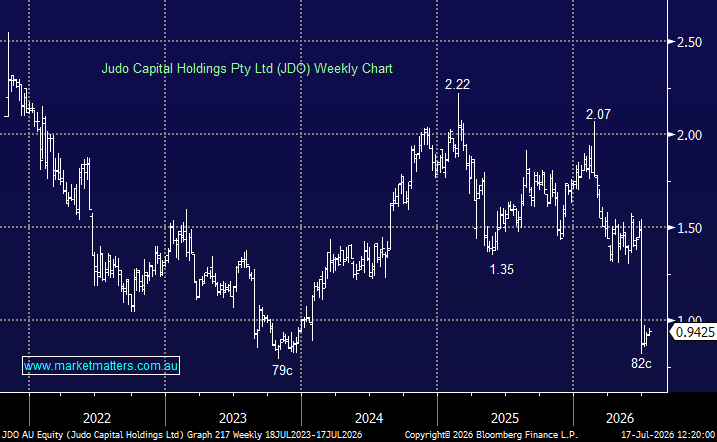

Judo Capital Holdings (JDO) – whether JDO is good value around 95c comes down to the health of small business in Australia, which doesn’t look good at present but that’s why the stocks trading below $1, down more than 50% from its 2026 high, after slashing FY26 guidance last month here on bad debt provisions.

One of our concerns is there are no analysts sell recommendations on the stock, with 75% Buys, i.e. the markets still positive. We would rather pay above $1 and see signs of stability in their loan book.

- We remain neutral JDO ~95c, it’s a coin toss to us.

Nine Entertainment (NEC) – NEC’s $850 million acquisition of QMS Media, completed in early 2026, is central to its portfolio transformation strategy. The deal was struck at 6.5x CY26e EBITDA and funded alongside the divestment of Nine Radio at 8.2x FY26e EBITDA, accelerating the group’s shift toward higher-growth digital assets, which are expected to contribute 60% of revenue and 70% of EBITDA from FY27.

The deal has been broadly viewed positively by the market, with analysts citing QMS’s premium street furniture and billboard inventory as an attractive proposition for ad buyers seeking bundled Total TV and out-of-home (OOH) exposure.

However, the acquisition has a meaningful near-term impact on dividend franking. The cumulative capital losses realised from the sale of broadcast radio assets and the QMS transaction are expected to reduce available franking credits. As a result, Nine Entertainment has indicated that its FY26 interim and final dividends, as well as the FY27 interim dividend, will be unfranked. Consensus DPS estimates are 7.2c in FY27, 7.8c in FY28 and 8.7c in FY29.

- We are neutral with a cautious positive bias towards NEC around 95c.