- What Matters Today in Markets: Listen here each morning or find all Market Matters Podcasts on Spotify.

The ASX200 again fought back from early losses on Thursday to finish down less than 0.1%, with the performance mantle being passed to the banks and retailers while the miners, and in particular BHP Group (ASX: BHP), weighed on the index – not great timing after we sung the praises of the “Big Australian” on Thursday morning! The materials sector took almost 36-points off the ASX200 after BHP and Evolution delivered a 1-2 of disappointing trading updates:

BHP Group (BHP) – On Thursday, BHP warned FY27 copper production could fall by up to 15% due to declining ore grades in Chile and an equipment failure at Carrapateena, with guidance around 2% below consensus – the stock fell 2.3% yesterday.

Evolution Mining (EVN) – On Wednesday, EVN warned inflation would materially lift FY27 costs, and will add 4–5% to FY2027 AISC; downgrades followed, sending the stock down 6.6% over the last two sessions.

The falls were a reminder that miners come with operational risk, whatever their quality. Neither were material enough “misses” for MM to reconsider our position, although frustrating nonetheless, and it appeared to weigh on the whole sector despite copper, nickel and iron ore firming this week.

The semiconductors experienced another frenetic, volatile session with the Korean KOSPI closing down -6.4%, although it remained well above Tuesday’s spike low. However, what caught our attention was that a standout result from Taiwan Semiconductor (TSMC US) wasn’t enough to stabilise the AI trade. Despite lifting FY26 revenue growth guidance to more than 40% and increasing capex to US$60–64bn on surging AI demand, the stock and broader semiconductor sector struggled, again illustrating the market’s “buy the rumour, sell the news” mood.

Overseas markets were mixed overnight with the AI trade continuing to weigh on parts of the market. In Europe, the UK FTSE advanced by +0.5% while the German DAX closed 0.3% lower. In the US, the NASDAQ tumbled 1.6% while the Russell 2000 small-cap index only slipped 0.1%.

- The SPI Futures are calling the ASX200 to open down 0.2% following the soft session on Wall Street and weaker commodities following the US launching its fifth straight day of strikes on Iran.

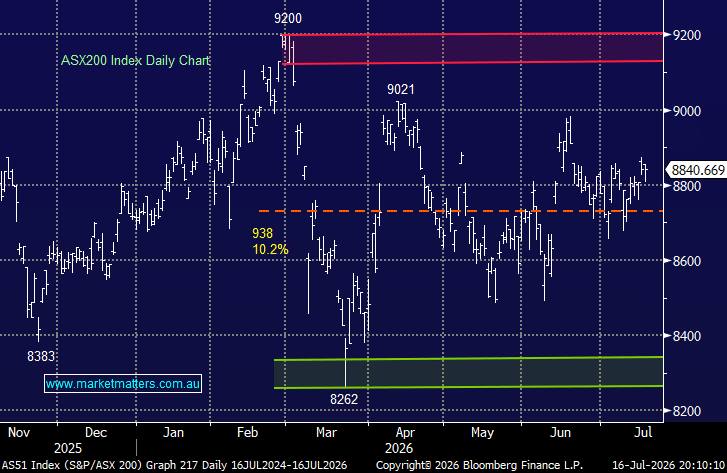

MM remains bullish towards the ASX200, around 8850

Add To Hit List