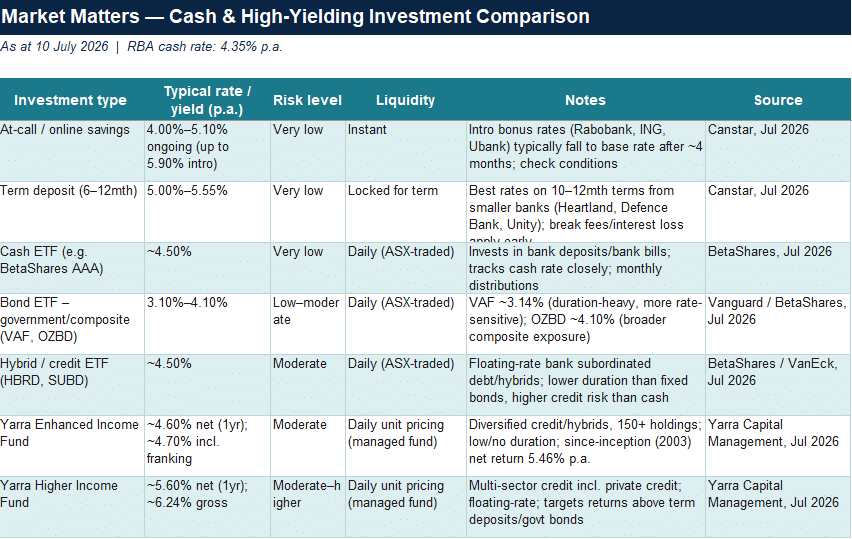

However, cash is no longer a one-size-fits-all asset class. Investors today can choose from at-call savings accounts, term deposits, cash ETFs, enhanced cash or floating-rate credit funds, traditional bond funds and private credit strategies, each offering a different balance between yield, liquidity and risk. At-call accounts provide maximum flexibility but typically lower returns, while term deposits generally offer a slightly higher fixed rate in exchange for locking money away. Cash ETFs such as AAA sit somewhere in between, providing daily liquidity, monthly income and returns that broadly track short-term interest rates, making them an efficient way to hold cash within a brokerage account.

For investors willing to accept more risk, enhanced cash and floating-rate income ETFs invest in investment-grade corporate debt and floating-rate securities, aiming to generate higher yields than cash with relatively low interest-rate sensitivity. Traditional bond funds and bond ETFs generally offer higher income again but carry greater duration risk, meaning prices can fall if interest rates rise. At the higher end of the risk spectrum sit private credit and income funds, such as those managed by Yarra Capital, Metrics, Realm or Qualitas. These strategies lend directly to businesses or property projects and typically target yields well above cash, but investors give up some liquidity and take on greater credit and manager risk in return.

Ultimately, the choice comes down to an individual’s requirements around liquidity, risk and return. Cash and term deposits prioritise capital preservation, cash ETFs add flexibility, enhanced cash and bond strategies seek higher income with modest additional risk, while private credit aims to maximise yield for investors comfortable locking away capital and accepting a higher level of credit risk.

The table below provides a quick overview. A few things worth flagging: the “yield” figures aren’t all measured the same way — bank/ETF rates are running yields, while the Yarra fund figures are total returns (income + capital), so they’re not perfectly apples-to-apples. Duration risk and credit risk both increase as you move down the table, which is why the higher headline numbers on hybrid/credit products and Yarra’s funds come with more volatility than cash or term deposits.