Hi Mark,

Two very different small caps with almost identical charts, so far in 2026 EOL has retreated ~30% and SPZ ~40%. However, they both are growth-oriented names trading at elevated valuations despite their YTD declines. EOL carries a higher valuation premium, reflecting its software/SaaS positioning in energy markets, while SPZ trades at a more modest multiple given its asset-heavier parking operations model.

Energy One Ltd (EOL): Energy One develops mission-critical energy trading and risk management software solutions for utilities, generators and retailers across Australia and Europe. the news flow over the year while relatively thin we believe had a net positive bias:

- 1H26 result: Shares rose ~10% after February’s 1H26 earnings, briefly trading above $15.50 before resuming their broader downtrend.

- CFO transition: CFO Guy Steel will depart on 31 August, with Jason Mabee joining as incoming CFO in July.

- European tailwinds: ICE’s decision to extend European energy trading hours to 21 hours per day should improve market liquidity and benefit demand for Energy One’s trading software.

- Regulatory positioning: The company continues to strengthen its position in European energy markets through REMIT 2.0 compliance solutions and its ISO 27001 cybersecurity certification.

Weakness over the last three quarter does appear correlated to the value compression across growth stocks and specifically those with software solutions. Importantly this $380mn business is profitable with adjusted net income nearly doubling from $3.4M to $5.9M between FY24 and FY25. Consensus expects it to nearly triple again to $17.6M by FY28.

However, its currently trading at ~41x FY26E EPS, a premium that reflects the growth profile but leaves limited margin for error, which explains the stock’s nervous trade.

- We like EOL in the $10-12 region.

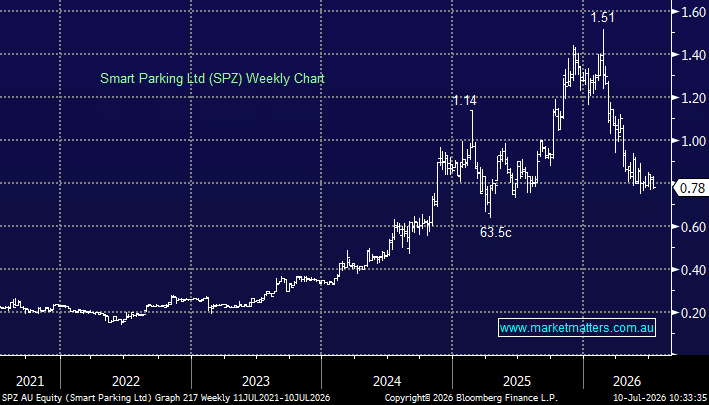

Smart Parking Ltd (ASX: SPZ): Smart Parking provides cloud-based parking technology, combining licence plate recognition, parking management software and payment solutions to help commercial property owners, retailers and local councils manage and monetise parking assets across the UK, Australia and New Zealand.

News was again net positive following its strong revenue beat in the 1H, but active US expansion caused acquisition-driven dilution which combined with broader small-cap selling pressure to weigh on the stock.

- 1H26 result: Revenue nearly doubled to $62.8m, comfortably ahead of the $53m consensus, although EPS eased to 1.02c from 1.11c.

- US expansion: SPZ acquired Oklahoma-based American Parking for US$12m, taking its US portfolio to more than 200 sites.

- Sector interest: EQT’s acquisition of rival Orikan highlights strong private-capital interest in smart parking, although it also points to rising competition.

SPZ is also profitable with net income forecast to more than double from $5.4M in FY25 to $12.9M in FY26E and nearly triple again to $26.7M by FY28E — a very steep earnings ramp driven by revenue scaling and margin expansion.

This $330mn stock is not expensive trading on 16.6x, especially considering the ~180% forecast EPS growth.

- We like the risk/reward towards SPZ between 60 and 70c.