- What Matters Today in Markets: Listen here each morning or find all Market Matters Podcasts on Spotify.

The ASX200 again fought back from early steep losses on Thursday to end down just 0.3%, reclaiming ~74% of its early deficit, but it still closed lower for the fourth consecutive day. The mining stocks again dragged on the index, with BHP Group (ASX: BHO) and RIO Tinto (ASX: RIO) making up almost 80% of the decline on their own, while this time it was more broad-based buying that supported the index rather than the banks that joined the miners on the wrong side of the ledger.

Over the last month, the healthcare (+16%) and consumer discretionary (+12%) sectors have both enjoyed double-digit gains while the previously high-flying energy (-7%) and materials (-6%) sectors have been the losers of the rotation. However, while this may be the start of broadening market gains both locally and overseas, we believe this wave of switching is likely coming to an end – the risk-reward towards some of the beaten-up healthcare/retail names isn’t as attractive now they’ve experienced a strong bounce.

- With copper bouncing (+2.3%) overnight, we feel some love is set to return to the influential ASX miners, e.g. overnight Freeport-McMoRan Inc (FCX US), which we own in the MM International Equities Portfolio, closed up more than +5%.

With no major economic releases due until next Tuesday night when we get US inflation data, most market attention will again be back on the US-Iran conflict which appears to be headed back down an all-too familiar path. However, it’s encouraging to see the oil price comfortable below US$80/barrel, still ~25% below its panic May highs as traders look past the current hostilities with a glass half-full attitude.

- We continue to believe stocks and bonds want to rally (risk on), but with the US and Iran trading air strikes, it’s going to be a test of July’s reputation as the ASX’s strongest month of the year.

Overseas markets were firm overnight despite geopolitical risks resurfacing, with the US and Iran trading airstrikes. In Europe, the German DAX and French CAC both ended the session up 0.9%. In the US, a bounce in semiconductors saw the NASDAQ gain +1.6%, helping support the S&P 500, which ended the session up +0.8%.

- The SPI Futures are calling the ASX200 to open flat despite BHP trading ~70c higher in the US.

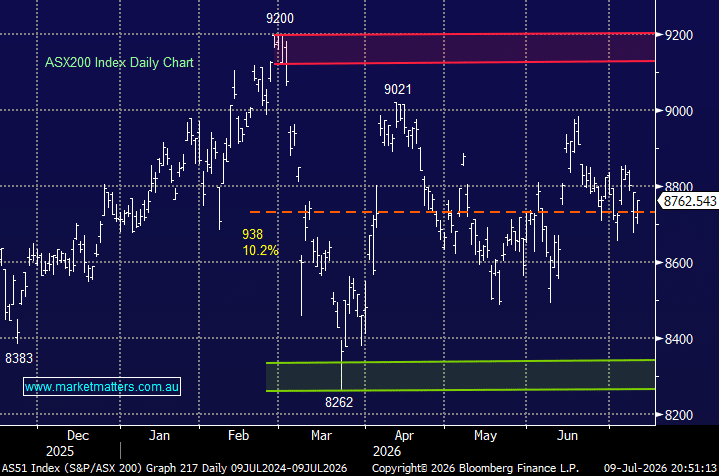

MM remains bullish towards the ASX200, around 8750

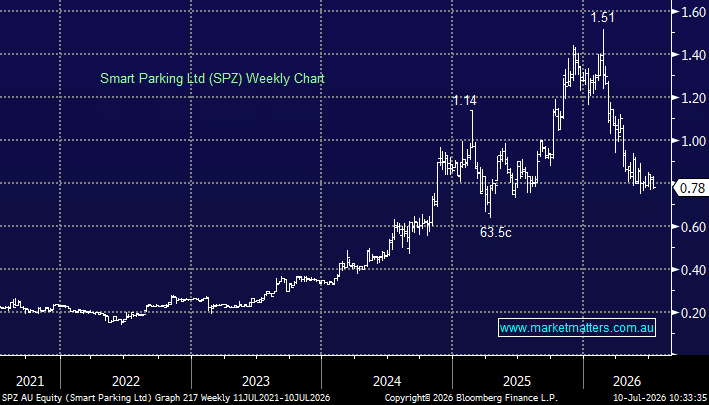

Add To Hit List