Suncorp (SUN) remains a core holding in the Market Matters Income Portfolio. The share price has enjoyed a solid run recently, but we continue to like the combination of improving earnings quality, attractive income and scope for further capital returns.

The latest trading update was mixed. Stronger investment markets are expected to lift FY26 investment income to around $750–800 million, comfortably ahead of previous expectations, prompting UBS to upgrade its FY26 earnings forecast by +6.7%. Catastrophe costs are also tracking around $200 million below budget, providing another tailwind into the August result.

The softer point was premium growth. Suncorp now expects FY26 gross written premium growth of 2.7%, below the roughly 4% indicated at the first-half result. Affordability pressures, greater competition and softer conditions in New Zealand are constraining customer volumes, particularly across Australian personal insurance.

This is worth watching because the recent insurance earnings cycle has benefited from substantial premium increases. As pricing moderates, future growth will need to come increasingly from customer retention, expense discipline and claims management rather than simply pushing through higher premiums.

- However, we think Suncorp is now a materially better and simpler business following the sale of its banking operations. It is a focused general insurer with strong brands, including AAMI, GIO and Vero, and greater capacity to return excess capital to shareholders.

The key near-term attraction is capital management. Suncorp’s new aggregate reinsurance cover should reduce earnings volatility and allow the company to operate with less surplus capital above its target range. We see scope for an additional $200 million buyback in FY27, with similar annual buybacks potentially sustainable in subsequent years.

The reinsurance structure is important because it provides greater protection against an unusually costly run of weather events. This should improve earnings confidence and may justify a modestly higher valuation over time, particularly as Suncorp narrows the protection gap with IAG.

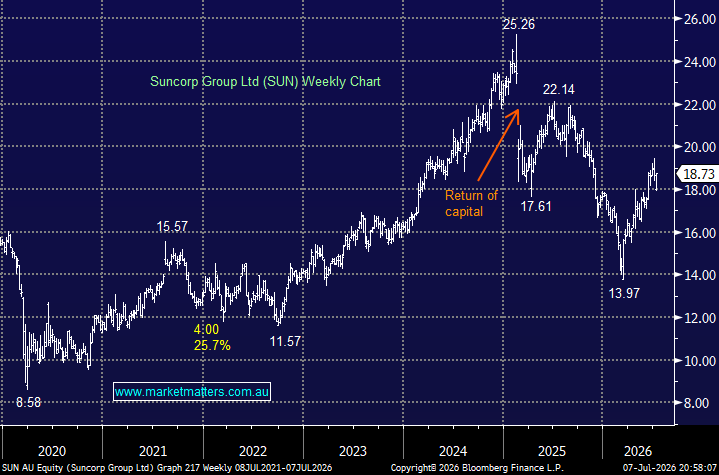

At around $18.70, Suncorp trades on ~15.4x forward earnings, broadly in line with its five-year average relative to the market and at a discount to IAG. We expect EPS growth of around 28% in FY27, supported by improved insurance earnings and capital management, while the prospective dividend yield rises toward 4.6% in FY27 and 4.8% in FY28.

The risks to this outcome would be a slowdown in premium growth, stronger competition, claims inflation and another period of elevated natural disaster costs. The recent rally also means the valuation is no longer as obviously compelling as it was earlier in the year.

The stock has had a reasonable run, and we would not chase it aggressively at current levels, but we still see a solid earnings and income profile. The combination of a growing ordinary dividend, potential buybacks and improved protection from catastrophe volatility makes it attractive for the Income Portfolio.

- We continue to like Suncorp and remain comfortable holding the stock, although a period of consolidation would not surprise us, i.e. the easy money is in the rear-view mirror.

MM remains bullish on SUN ~$18.70

Add To Hit List