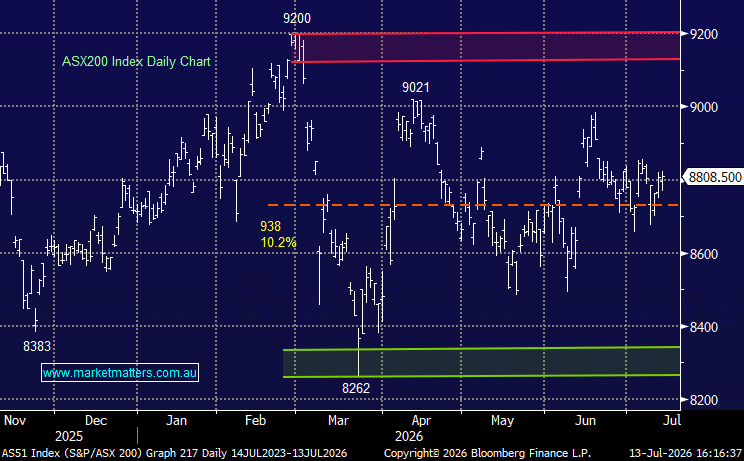

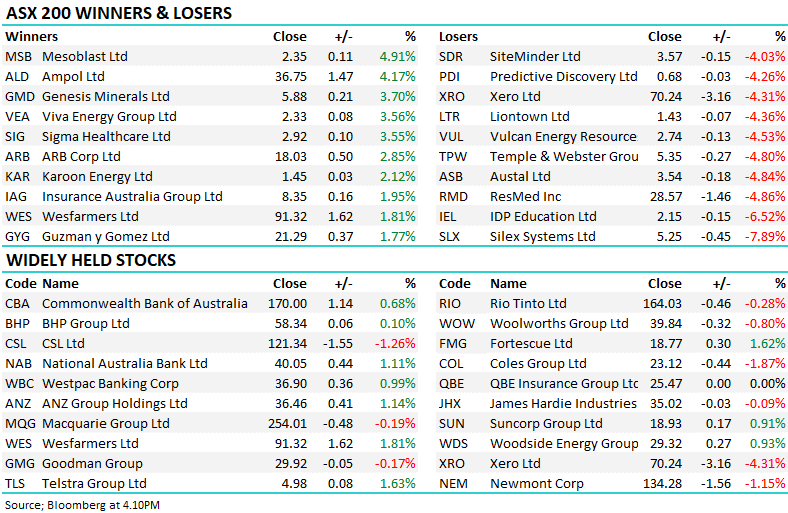

Australia’s largest supermarket operator is up +38% so far this year as it recovers strongly from the uncertainty around the price-fixing investigation by the ACCC. The company’s actually had a mixed year operationally at a glance, firstly delivering a strong earnings beat in February only to deliver a mild profit warning in April due to rising costs and increased customer caution.

In our opinion, WOW is well positioned to benefit from the evolution of AI, a narrative we discussed in detail here. Having enjoyed a strong end to the FY, Woollies isn’t cheap at current levels, but we feel its steady growth and potential to lift margins justifies its current valuation. If we were long, we would see no reason to exit, and from a defensive element to a portfolio, it’s attractive.

- We can see WOW making new highs in 2026, now only ~5% away.

MM is bullish towards WOW around $40

Add To Hit List