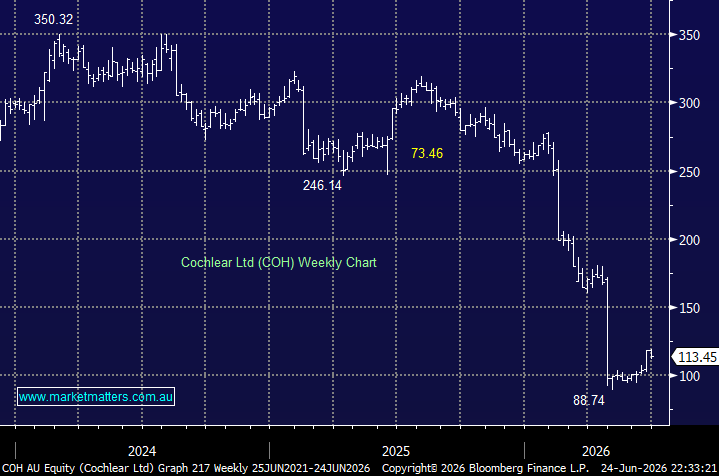

COH has delivered two painful downgrades in 2026, taking the stock down 56% just this year. We covered Aprils savage downgrade here, coming to the easy conclusion that this was a stock best avoided for the foreseeable future, especially if we remember the market adage, “Buy the Third Downgrade.” Two downgrades in three months do not breed confidence in a market that’s very comfortable throwing stocks into the naughty corner and forgetting about them.

COH is a very similar story to CSL from a valuation contraction perspective, with it also trading ~50% below its average valuation of the last 5-years. However, with the stock now looking to deliver flat revenue between FY24 and FY27 its doesn’t deserve to be priced for growth.

- We see no reason to chase a bounce in COH above $110 from an investment perspective – preferring to wait for their FY26 results due in August before re-assessing. We wouldn’t be surprised to another (smaller) cut to guidance.

MM is neutral towards COH around $113

Add To Hit List