Hi John,

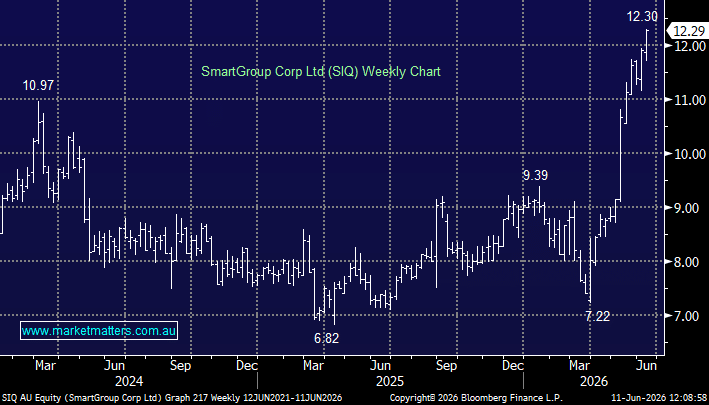

SmartGroup (SIQ) provides salary packaging, novated leasing and employee benefits administration services across Australia. As you alluded to, the $1.7bn salary packaging and novated leasing provider has surged ~70% from its March lows as the market rerates the stock on the back of accelerating EV novated leasing demand, favourable policy settings and growing confidence in the company’s earnings trajectory.

- In Q1 2026, novated lease orders increased +22% year-on-year, with management citing strong demand dynamics.

The EV fringe benefits tax exemption introduced by the Albanese government has been a genuine gamechanger for SIQ’s business model. Being one of Australia’s largest novated-leasing platforms, it has meaningful exposure to accelerating EV adoption. Traditionally, this lower growth business that was susceptible to government regulatory change was priced on a low double digit PE, however, as the level of growth has increased, the multiple has also gone up, amplifying the share price gains.

While policy risk appears limited in the near term, the outlook beyond 2028 warrants close attention. The EV Fringe Benefits Tax exemption has been a major growth catalyst for SmartGroup, meaning any future policy changes could have a meaningful impact on earnings expectations and valuation. It’s not a pressing concern today, but one investor’s should keep firmly on the radar.

However, for now, the backdrop remains highly supportive, with elevated fuel prices following the Middle East conflict likely to further enhance the relative attractiveness of EVs and underpin demand for novated leasing solutions.

- SIQ is a rare stock to benefit from both government policy and the US-Iran war.

We did own this stock, and sold way too early. If we still held, we’d at least be trimming the position after the run up – 18x for this sort of business is now expensive in our view.