Hi Debbie,

We’ve already covered SmartGroup (SIQ) elsewhere today, so we’ll focus on Perenti (PRN).

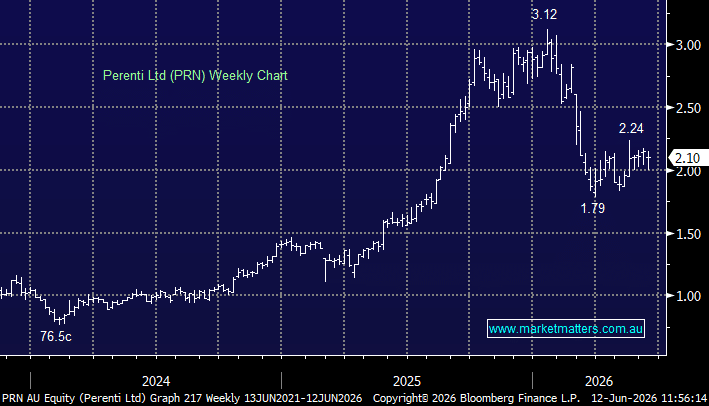

Perenti is a mining services contractor that provides underground mining, drilling and mining support services to resource companies globally. Unlike the miners themselves, PRN gets paid to build, drill and operate mines for others, making earnings more dependent on mining activity and capital expenditure than commodity prices directly.

Operationally, the ~$2bn company continues to perform steadily. In H1 FY26, Perenti delivered record earnings (Ebitda) of $160m on revenue of $1.73bn.

The market’s concern wasn’t the result itself, but what comes next. The completion of a major contract in Botswana has created a near-term earnings headwind, and investors are waiting to see how quickly management can replace that work through new contract wins. In other words, the market is looking beyond the record result and focusing on the sustainability of future earnings.

Adding to the uncertainty is the recent CEO transition, with Dr Vanessa Torres formally taking the reins on 1 June. While we view the appointment positively, leadership changes often create a period of “wait and see” for investors.

The valuation looks attractive on paper (10x), but we’d want to see evidence that the contract pipeline can offset the Botswana roll-off, alongside early signs of strategic execution under the new CEO.

- At around $2, we remain neutral.