Insurance is a good business when pricing is disciplined and claims are benign, but natural perils can quickly change the earnings profile in any given year. That was evident in the first half for SUN, where elevated catastrophe claims pushed reported insurance trading margins to their lowest level in more than a decade – and they were forced to cut the dividend.

Last week, Suncorp moved to materially reduce that volatility. The company has taken advantage of improving reinsurance market conditions to put in place a new five-year aggregate reinsurance program, providing $2.4bn of cover in total, or an average of ~$480m per annum, with a maximum recovery of $800m in any single year. The cover is designed to sit just above Suncorp’s catastrophe budget, meaning the company is effectively paying up to cap the downside in more difficult claims years. UBS estimates the structure should cap losses at that level in around 90% of scenarios.

There is a cost to this. Estimates of the deal imply this could reduce FY27 net earned premium by around 1.6%, and it trims its FY27/FY28 EPS forecasts by ~1–2%. However, that is not the way we think investors should assess it. For a stock held in our lower risk income strategy, a modest earnings headwind is a very reasonable price to pay for a material improvement in earnings visibility, lower capital volatility and a more predictable dividend profile.

Suncorp has become a cleaner, lower-risk general insurer. The bank has been sold, the balance sheet is more focused, and management is now actively reducing the major swing factor in the business – catastrophe volatility. Importantly, despite the higher reinsurance spend, Suncorp continues to indicate that underlying insurance trading margins should remain toward the upper end of its 10–12% target range, which speaks to the strength of pricing, cost discipline and the broader insurance cycle.

While this change does not make Suncorp immune to weather events, it does reduce the chance of a bad claim’s year derailing earnings, which has been the case recently. We expect Suncorp’s dividend yield to move back above 5% in FY27 and FY28 following a lower FY26 payout, with the interim dividend of 17cps dragging down the FY payout to ~4% (we’re expecting 45cps for the final dividend in August).

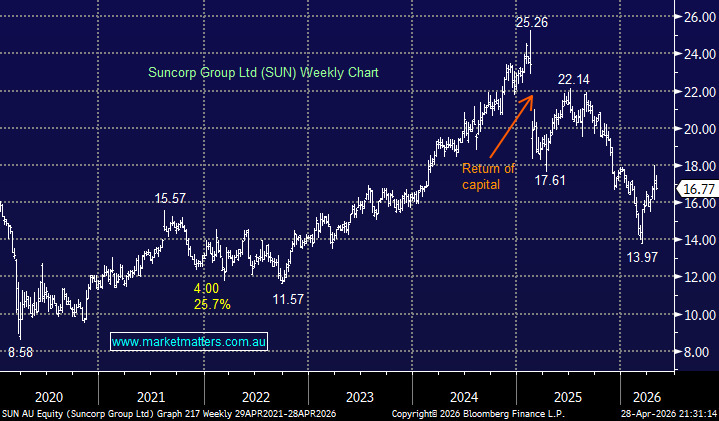

- We liked the announcement last week from SUN, and it increases our conviction in the stock within the Income Portfolio.

MM remains long & bullish SUN

Add To Hit List