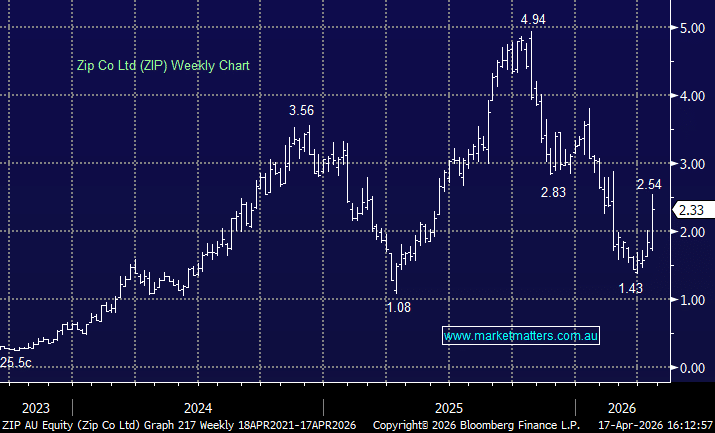

ZIP +13.66%: Surged today, after a strong 3Q update and upgraded earnings outlook, reversing some of the heavy selling the stock has endured in recent months alongside the broader tech and payments sector.

- Revenue: $332.2 million +43% y/y

- Transaction volume: $3.99 billion +22% y/y

- Active customers: 6.5 million +3.5% y/y

- Merchants: 93,900 +13% y/y

- FY26 cash EBTDA guidance of more than $260 million

The key catalyst was the upgraded profitability outlook, with the company now expecting FY26 cash EBTDA of at least $260 million, a meaningful step up following February’s update that suggested flat second-half earnings growth — an announcement that triggered a sharp selloff at the time.

Operationally the business continues to show strong momentum in the US, where Zip expects TTV growth greater than 40% in USD terms, alongside improving margins and declining credit losses. Management also flagged group revenue margins of around 8% and operating margins above 18%, with credit losses in the US expected to fall below 1.75% of TTV by the June quarter.

ZIP has been caught in the recent tech-led weakness and concerns around AI disruption to payments, so the strong earnings update provided a sharp reset for sentiment.

MM is long and bullish ZIP

Add To Hit List