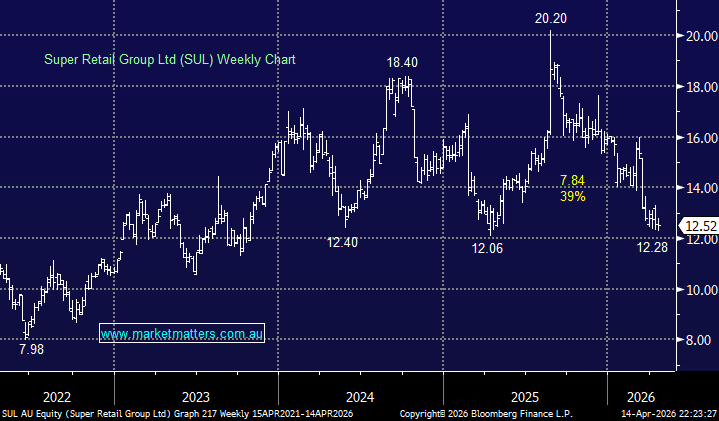

SUL has delivered two strong results since last August ’25 but economic conditions have weighed on the stock, we liked Februarys result Here. This is a company MM likes and we held the stock in both our Active Growth & Income Portfolios through 2025, managing to take a profit on both as the sector crumbled with the RBA adopting a hawkish stance on interest rates.

Our recent note on SUL still holds up, the stock looks good value trading one standard deviation below its 5-year average valuation although we currently prefer JB Hi-Fi (ASX:JBH) in the sector for yield, though it’s a close race. They key here is when MM decides the economy is turning and we want to increase our retail exposure with SUL the likely candidate – the consumer discretionary sector makes up 7-8% of the ASX200 and currently we only hold 4% in JBH allowing plenty of room to add SUL before considering moving overweight the sector.

As we mentioned earlier stocks tend to lead the underlying fundamentals with yesterdays consumer confidence numbers clearly telling us SUL’s customers are doing it tough. We need a catalyst before increasing our retail exposure at this stage but with the sector already down 25%, and SUL 40%, from their 2025 highs plenty of “bad news” is built into the share prices – it feels too early but the sector is far closer to low than a top.

- We like SUL for its estimated ~7.3% fully franked yield, assuming trading conditions don’t collapse.

MM is cautiously bullish towards SUL around $12.50

Add To Hit List