- What Matters Today in Markets: Listen here each morning or find all Market Matters Podcasts on Spotify.

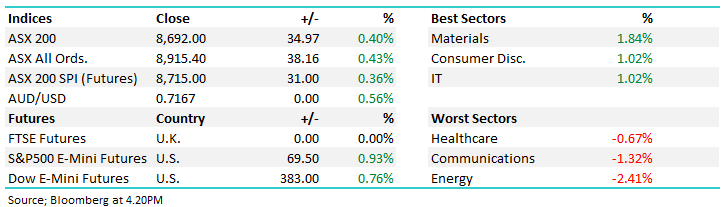

The ASX 200 bounced another +0.6% on Wednesday with the miners and banks dragging the market higher, even when only 45% of the main board closed in positive territory. To put things into perspective, the local bourse closed up 50-points with the miners alone contributing +42 points to the day, helped by another solid day for iron ore, and related names. Traders were offered some relief from the recent volatility spurred by the Iran war on Wednesday after the International Energy Agency (IEA) reportedly proposed the release of oil reserves. Unfortunately, the market failed to follow the heavyweight sectors higher, with weakness resurfacing in the tech and high growth stocks, more on this later with the Tech Sector, closing down 1.6%, just missing out on the wooden spoon to the Utilities sector.

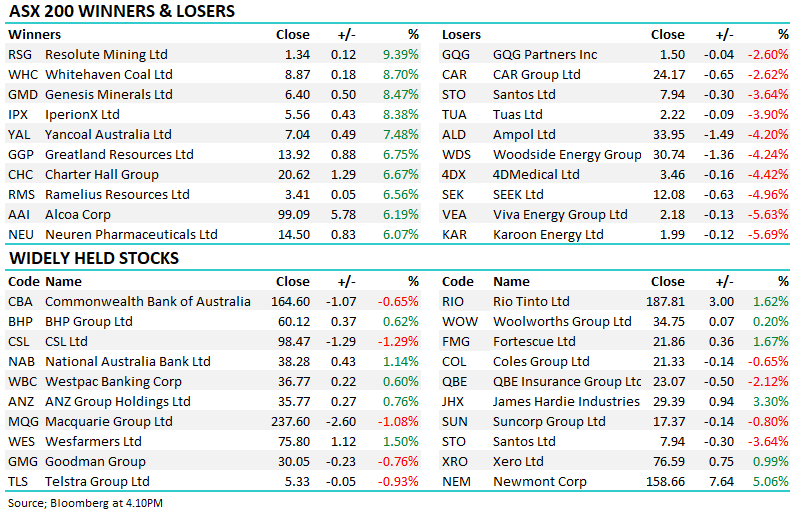

- Iron Ore closed back above $US104/MT on Wednesday, over 6% above its February high and well above the consensus view of ~$US94 by year-end.

Domestic headlines were dominated by growing expectations of a March rate hike. RBA Deputy Governor Andrew Hauser warned that failing to act decisively risks embedding inflation expectations, potentially leading to persistently higher inflation. Westpac now expects the RBA to hike by 25bps in both March and May, taking the peak cash rate to 4.35%, as policymakers respond to a temporary lift in inflation driven by higher oil prices. BofA and others also sees a March hike, noting inflation remains above target and the labour market is still tight – we now agree and expect the RBA to move on the 17th.

- Futures markets are now pricing in a 65% chance of a hike next week and a minimum RBA Cash Rate of 4.35% come Christmas.

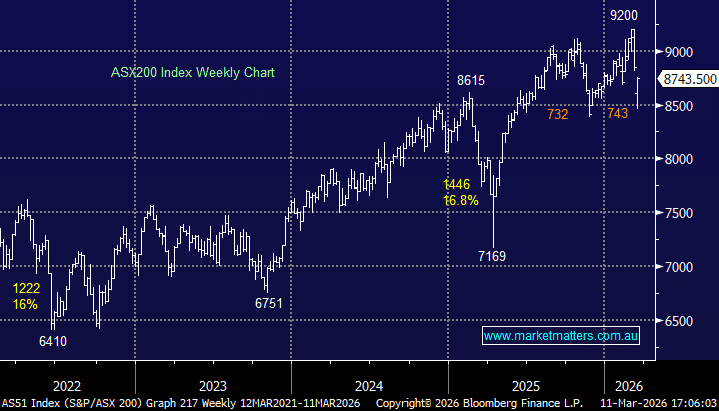

So far, March has delivered a 743-point pullback, mirroring the move through October/November of 2025 – it’s why MM is always conscious of the market’s recent rhythm. However, we are not yet convinced that Monday’s low is the end of the current pullback, especially for some stocks/sectors in the current extremely polarised market.

Overseas markets were soft overnight on war jitters as oil continued to trade above $US90, with the largest ever release of emergency reserves being seen as just a reprieve as the war in Iran drags on. In Europe, the German DAX fell 1.4% and the UK FTSE 0.6%. In the US, a relatively quiet session saw the S&P 500 retreat 0.1%, and the Russell 2000 small-cap Index -0.2%.

- The SPI futures are calling the ASX200 to open down 0.5% with the miners likely to weigh early with BHP down 70c in the US.

MM is now bullish towards the ASX200 around 8750

Add To Hit List