Uranium producer Paladin Energy (PDN) operates in Namibia and boasts a growth pipeline in Canada, offering clear leverage to strengthening global nuclear demand. It’s the last position in our Active Growth position whose report we need to cover, primarily as most things came in line, and the share price reaction was relatively small.

PDN reported a gross profit of $US26mn for the 1H, a significant increase from the previous period. The loss after tax of $US6.6mn was driven by ramp up of its Langer Heinrich Mine (LHM) mine in Namibia, business expansion following the Fission Uranium Corp acquisition (now Paladin Canada Inc) and TSX listing and financial activities.

1H26 Highlights:

- Net Income $0.87mn v loss of $4.57mn YoY.

- Revenue of $138.3mn, +79% YoY.

- Cash and cash equivalents of $121mn, +36% h/h.

This was a solid result with no hidden surprises, and Paladin’s ramp-up at LHM continues to track well, with additional mining fleet arriving on site and stronger contract pricing driving a sharp lift in half-year sales. Meanwhile, the Patterson Lake South (PLS) project in Canada progressed following the recent $300m equity raise and $100mn SPP, positioning the group for its next leg of growth. Management also moved to tidy up the balance sheet, reducing drawn debt and boosting available liquidity. The company now enjoys meaningful funding flexibility.

A week after the result, PDN rallied ~5% on the 20th Feb after announcing they had secured ministerial approval for the environmental impact statement (EIS) at its PLS uranium project in Canada, a critical prerequisite for progressing provincial and federal permits and licences toward construction. With the EIS cleared, the company can now advance the construction licence process with the Canadian Nuclear Safety Commission (CNSC). To put things into perspective, while the PLS project is not a top-three global asset, it is a sizeable, high-grade, globally relevant that will make Paladin a more material uranium player once built, with production aimed for the early 2030s

After a really tough 2024 and start to 2025, PDN has turned itself around operationally, in a well-timed fashion, just as the uranium price turned higher. The stock has already surged more than +350% in less than 12-months helped by some fairly aggressive “short covering” – Its short position has fallen from ~19% to sub 10% as its forced its way up the ladder in uranium ETFs such as the URNM, where its now the 4th largest holding behind Cameco, Uranium Energy Corp and Sprott Physical Uranium.

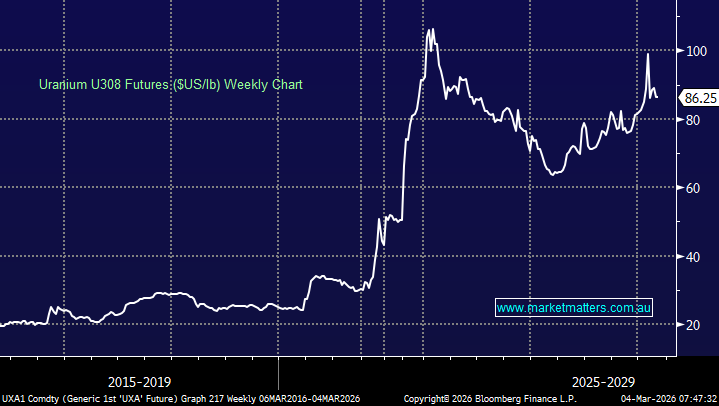

Uranium futures are trading around $US88/lb, consolidating after pulling back from January’s two-year high of $US101.50/lb. Yellowcake remains almost 10% higher year-to-date, underpinned by a constructive demand outlook. Momentum on the demand side continues to build, led by power-intensive data centres, with several US tech giants signing agreements linked to small modular reactor (SMR) development. Policy support has also strengthened, with the US streamlining regulations for uranium conversion and enrichment and backing new reactor construction. Notably, partnerships involving Cameco and Westinghouse reactor development have progressed, while $US2.7bn in fresh contracts have been awarded to Centrus and other nuclear fuel and enrichment groups to reduce reliance on Russian supply following sanctions.

The World Nuclear Association’s 2025 reference sees demand rising to ~390Mlb by 2040, incorporating all known projects and depletion from existing mines. Modelling points to a structural deficit that widens materially next decade, with the market potentially short more than 200Mlb by 2040 unless significant new supply emerges. The coming uranium supply deficits could become the rate limiter for nuclear power generation, hence we can see a significantly higher uranium price in the coming years.

- We remain bullish towards uranium over the coming years in line with our view that the nuclear fuel is entering a bullish Supercycle.

PDN, like the whole uranium sector is a volatile beast and although its surged higher over the last year it’s also experienced three corrections of around 25%. Hence, we may trim our position back towards our target 4% if/when the miner tests $15, but we have no intention of losing our exposure to the nuclear story for the foreseeable future.

- We continue to like PDN but may trim our position into new highs for 2026: MM owns PDN in its Active Growth Portfolio.

MM is long and bullish PDN

Add To Hit List