SUL +8.39%: shares rallied after the retailer delivered an in-line 1H result but, more importantly, pointed to a clear improvement in trading momentum early in the second half.

While headline earnings were down year-on-year, there was evidence that trading conditions are stabilising and, in some categories, improving. Group like-for-like sales rose 3.5% in the first six weeks of 2H, driven by strength in Supercheap Auto and BCF, helping to ease concerns which had be obviously across the market – MM included.

1H26 Highlights

- Underlying NPAT $121.9m, down a more modest 6.9% y/y, but inline consensus

- Group revenue +4.2% to $2.19bn; comparable sales +2.5% – inline with consensus

- Interim dividend of 32c maintained

SUL showed strong cash generation, disciplined inventory management, and improving like-for-like sales implying SUL has navigated the worst of the margin and demand pressures seen over the past 12 months.

In contrast to other discretionary retailers still grappling with weak foot traffic and elevated discounting, SUL’s exposure to auto and leisure categories, areas where consumers continue to spend despite broader caution, was supportive.

- Overall, earnings were soft, but the outlook is improving.

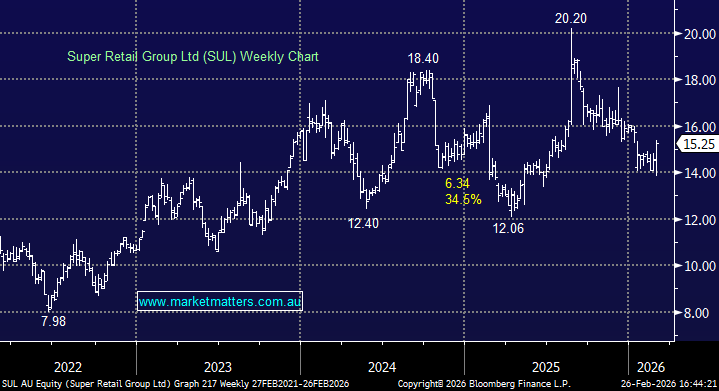

MM is neutral SUL ~$15, still preferring JBH at current levels

Add To Hit List