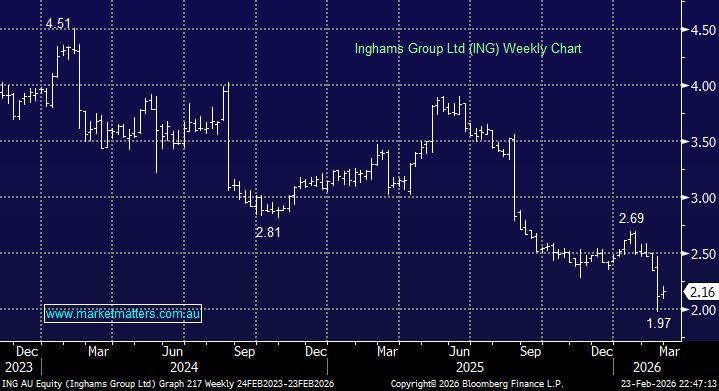

Poultry giant Inghams plunged as much as 19% to an all-time low after downgrading its FY26 earnings due to delays in operational improvements.

- Inghams downgraded FY26 earnings guidance (EBITDA) by 15% to $180-200mn.

This was, without doubt, a clear miss, and the market’s reaction was in keeping with current sentiment. The company said, “The measures that have been implemented are taking longer than initially anticipated to translate into financial results and are now expected to be more heavily weighted towards the final quarter of FY26.” In other words, cost-out timing disappointment, not demand destruction. But assuming as we are its just a timing factor, the stock is looking attractive at the current level, trading on an undemanding valuation, especially considering the confidence of CEO ED Alexander:

- The CEO said there were “clear actions in place” to reduce supply chain costs and improve operations, which would boost performance in the second half of the financial year. “While the first half is disappointing, a return to positive top-line growth and improved operational foundations means that we are well positioned for improved earnings momentum into the financial year 27.”

At current levels, ING offers a high dividend yield and is priced as though margins will never recover, a scenario that looks overly harsh given the structural position of the business. Volumes have remained broadly stable, pricing in wholesale channels is beginning to show early signs of improvement, and management continues to guide to a recovery into FY27 as cost initiatives progressively flow through. Poultry demand remains defensive in nature, particularly as consumers trade down from higher-priced proteins.

- We believe ING’s valuation (Est PE of 11.4x) looks interesting, with its ~5.6% fully franked yield allowing investors to be patient. Bottom feeding in INS has not been a winnings strategy in recent times; however, we now believe current levels are pricing in a “scorched earth” scenario.

MM is bullish ING around $2.10

Add To Hit List