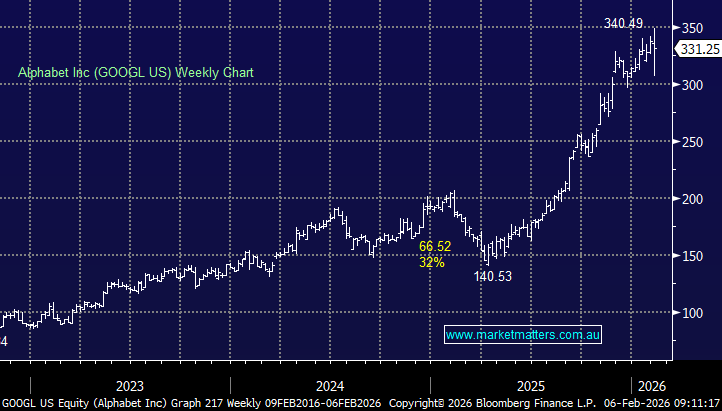

Alphabet shares were mildly lower overnight after flagging FY26 capex of $175–185bn, well above consensus (~$120bn). The spending shock overshadowed a clean earnings beat, with Search and Cloud both accelerating as AI demand lifts utilisation and pricing power. The debate is simple: near-term free-cash-flow pressure versus longer-term AI leadership.

4Q highlights

- Revenue ex-TAC: $97.2bn (+19% y/y) beat

- EPS: $2.82 vs $2.65 beat

- Total revenue: $113.8bn (+18%) beat

- Google Search & Other: $63.1bn (+17%) beat

- YouTube ads: $11.4bn (+8.7%) miss

- Google Cloud: $17.7bn (+48%) beat

- Cloud operating income: $5.3bn (vs $3.7bn est.)

- Capex: $27.9bn (inline); FY26 guide far above Street

Google is clearly pressing its advantage as AI workloads surge, ramping up capex materially. Citi / Jefferies / Evercore all write that results show AI investments are paying off and that while capex is aggressive, it will support growth.

Ultimately, Google is creaming it, and could well be the primary winner in AI, but we don’t know at this stage. There is a lot of upside built in at current levels, and our preference is to revert to a neutral stance in the short term.

MM has turned neutral toward GOOGL, sold at ~US$323 in the International Equities Portfolio overnight

Add To Hit List