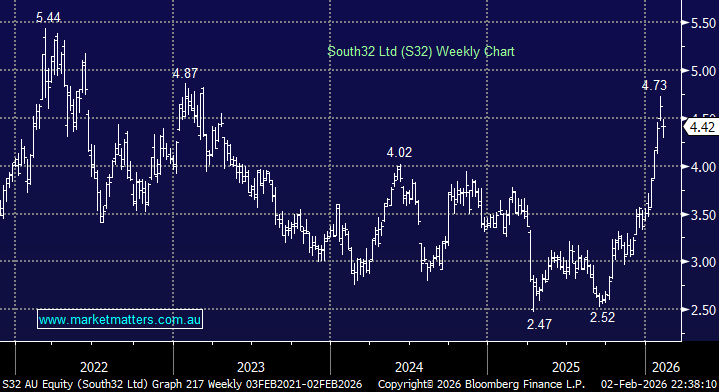

Volatility has been extreme in precious metals of late, but in the bigger picture, we can see deficits and declining inventories suggesting silver is now increasingly vulnerable to periods of strong investment demand, which in turn could lead to further bouts of liquidity tightness. S32 is exposed to silver through its 100% interest in the Cannington mine in QLD, which produces silver, zinc and lead, and is one of the top 10 silver mines globally. While the stock has had a very strong run – and has simply come off the top – we do think opportunities will arise in the current volatility, even if it’s not in the coming days.

More so than Silver, Aluminium+ Steel related related commodities are central to S32’s earnings base – Bauxite, Alumina & Aluminium – while it’s also one of the world’s largest manganese producers, along with exposure to Met Coal, making S32 very leveraged to steel demand, which is a theme we like based on the global shift towards decarbonisation, but with less exposure to bulk iron ore than peers like BHP or Rio, that have a potential headwind from rising global Iron Ore supply.

It is however, important to recognise that S32 tends to be more cyclical than the majors, because aluminium pricing is energy-sensitive given the high draw from smelting.

- We believe S32 will be volatile over the coming months, but this is one miner that we don’t own, that would look attractive into weakness.

MM is bullish towards S32 around $4.20

Add To Hit List