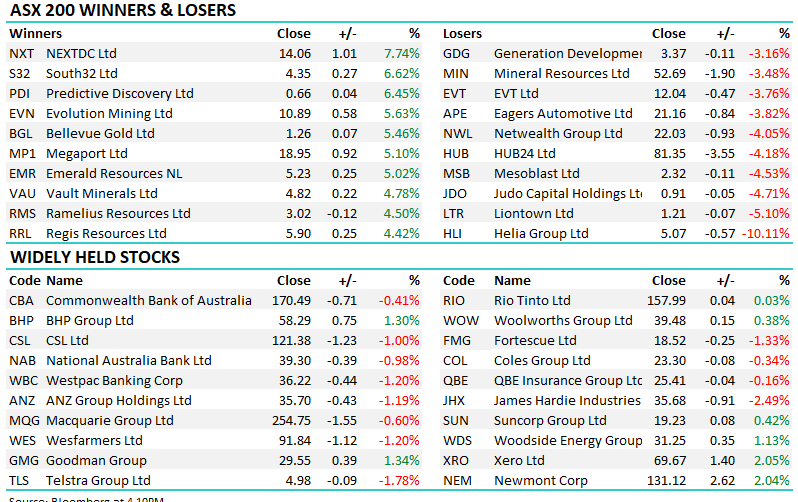

US indices enjoyed a strong session overall as they awaited news from the Fed’s two-day FOMC meeting, which commenced overnight. Nvidia (NVDA US) was the focus of much attention following their first GTC conference, although the stock itself was relatively quiet, i.e. the global artificial intelligence conference might become the new go-to for live events, replacing Apple Inc (AAPL US) and Warren Buffett’s Berkshire’s eagerly awaited presentations. The Fed is expected to keep rates unchanged tonight, but after the recent robust economic data, investors have been concerned that Jerome Powell will signal that interest rates will remain higher for longer – as we touched on earlier, we can see the “rate cut can” being kicked down the proverbial road a few times in 2024.

- We are cautiously bullish about US stocks, but further consolidation looks increasingly likely after the strong gains since late 2023.

MM remains cautiously bullish towards US stocks

Add To Hit List

Rate cuts don’t mean stocks rise, and vice versa, a fact perfectly illustrated by Japan’s Nikkei over recent months, which surged higher even as the first rate hike in 17 years was increasingly priced into financial markets. Even after outstripping most equity markets over the last 12-months Goldman Sachs believes Japanese equities are set to rise further due to two important structural changes unfolding, i.e. The country is shifting to an inflationary economy after years of deflation, and corporate governance reforms are taking root helping investor confidence gather momentum.

- We can see a period of consolidation around the 40,000 area, but surprises are always likely with the Nikkei’s trend on the upside.

MM is bullish towards Japanese equities in the medium term

Add To Hit List