The US trod water overnight as the market braces for an avalanche of economic data and heavy Treasury and corporate bond sales as we approach month-end with about $US35bn of fresh offerings expected this week. Thursday is likely to be key this week as the Fed’s favourite inflation read, the core personal consumption expenditure price index, is released, with markets expecting a strong number that will validate the Fed’s recent steadying rhetoric. Under the hood, Alphabet (GOOGL US) fell over 4% while underperforming Tesla (TSLA US) bounced +3.9%.

- The broad-based US Russell 3000 Index remains around all-time highs providing no sell signals for the vocal bears.

MM is neutral towards US stocks short-term

Add To Hit List

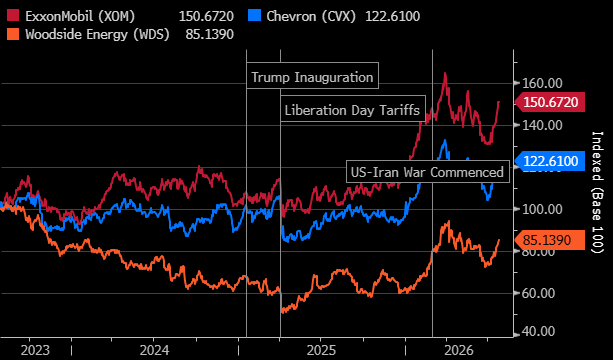

Oil prices rallied over +1% overnight as the volume held in floating tankers fell by 7.5%, and demand from China showed signs of finally picking up. However, trading volumes were muted as several participants attended International Energy Week in London. The small gain was enough to help the US Energy Sector to a +0.3% advance in the lacklustre session.

- Oil has been trading at around the $US80 a barrel level since late 2022, and we see no reason to fight the sideways trend until further notice.

MM is neutral towards crude oil

Add To Hit List