What Matters Today in Markets: Listen here each morning or find all Market Matters Podcasts on Spotify.

Yesterday, the Peoples Bank of China (PBOC) announced lenders had cut their 5-year loan prime rate (LPR) by 25 basis points to 3.95%; it was the first cut since June, reaffirming Xi Jinping’s intentions to reinvigorate their economy, which the prolonged property crisis has weighed down. This was the biggest-ever cut to the key mortgage reference rate as Chinese banks cut rates to incentivise borrowing; the targeted stimulus will increase the potential pool of buyers as apartment prices continue to slip lower.

- MM continues to believe that Beijing will deliver ongoing targeted stimulus through 2024, support we believe must eventually stimulate growth.

Interestingly, after several false dawns over the last 12-months, the rate cut failed to impress investors – we believe it might be the very time they should take notice. The cut in the LPR was the largest since the reference rate was introduced in 2019 and far more than expected, but this time, investors sold into any strength on the day as opposed to 24-48 hours after the stimulus, i.e. the Shenzhen CSI 300 index advanced just +0.2%.

The latest BofA fund manager’s survey, completed on the 8th of February, showed global players are still very bullish on equities and, especially tech & the “Magnificent Seven”, but short Chinese equities remain the second most crowded position after bullish bets on Microsoft, Nvidia, Meta Platform et al. We believe it’s a matter of when, not if, we see an aggressive squeeze higher by Chinese stocks – a bullish read-through for the Resources Sector, that is so far not listening to our view.

- The lacklustre performance by Chinese stocks could be the calm before the storm; we still believe the next ~20% move is on the upside.

MM remains bullish towards Chinese equities

Add To Hit List

Yesterday’s earnings numbers and accompanying general news had little impact on the ASX200, which closed marginally lower. However, we still saw 7% of the index up/down by over 5% while losers just outnumbered the winners. We’re getting used to the extreme volatility on the stock level this reporting season, and there is still plenty to go with RIO Tinto (RIO), Lovisa (LOV), Iluka Resources (ILU), Calix (CLX), Woolworths (WOW) and Santos (STO) all facing the music today – hold on tight, it’s been a bumpy ride so far!

On the sector level, it was yet more reversion with the Materials and Energy Sectors weighing on the index while Real Estate and the Financial stood out in the winners’ enclosure, the opposite to Monday! Suppose the aggressive move by the PBOC gains traction over the coming days/weeks. In that case, we should see the Resources Sector enjoy a bid, but selling any bounce in China has paid dividends over recent years, and trends do have a habit of lasting longer than many expect.

Overnight US markets slipped lower as profit-taking rolled the much-loved major tech names led by NVIDIA (NVDA US), which finished down -4.4% ahead of its key earnings figures tonight.

- This morning, the SPI Futures are pointing to an early decline of -0.3% with BHP Group (BHP) down~15c in the US.

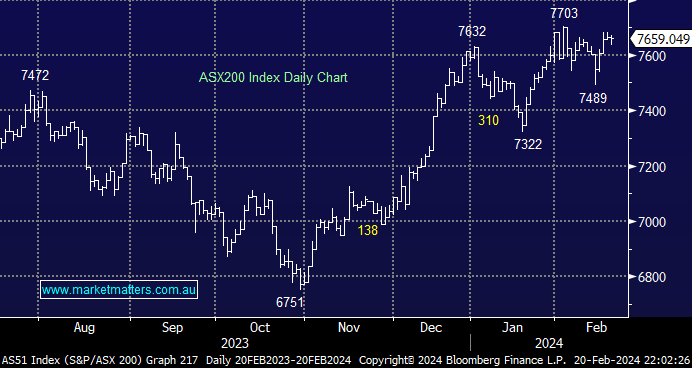

MM is now neutral toward the ASX200 in the 7600 area

Add To Hit List