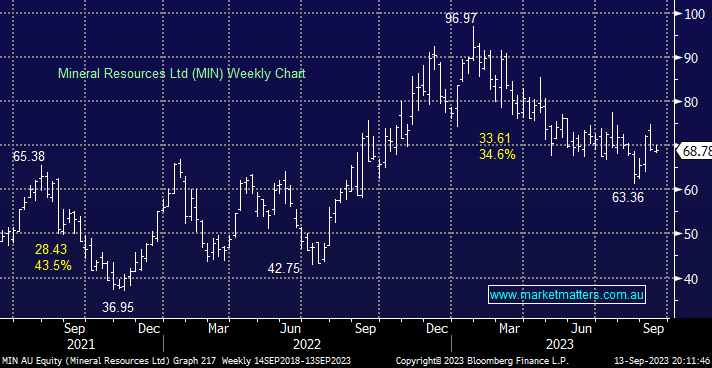

Iron ore and lithium miner MIN only slipped -0.7% yesterday, outperforming other names in its core sectors. The company reported well in August beating on the profit line by ~6%, plus the 7c fully franked dividend was higher than most analysts had forecast. At this stage of the cycle, we don’t believe MIN is being credited with the potential upside for iron ore above $US120/tonne, plus the almost inevitable turnaround by lithium prices. From an exposure perspective, in 2023, 45% of their revenue came from iron ore and 40% from lithium, while the balance of ~15% came from mining services – as subscribers know we like the China thematic which should continue to support iron ore prices in the short term at least, while their Lithium exposure provides a strong longer term tailwind MIN.

- We will consider increasing our MIN position under $65 – MM owns MIN in our Flagship Growth Portfolio.

MM remains long and bullish towards MIN

Add To Hit List