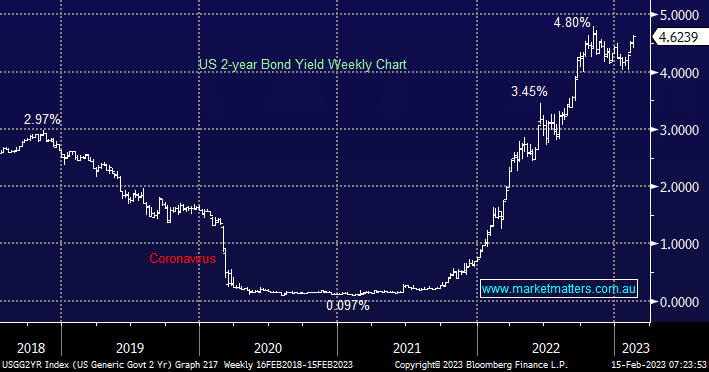

US stocks largely shrugged off another hot inflation number overnight with the CPI printing 6.4%, above analysts’ estimates of 6.2%. The Fed comments were mixed from a couple of officials but importantly swaps markets are now pricing in a 50% chance of a +0.25% rate hike in June, following jumps in both March & May, hence the US 2-year yield increased another 0.1% breaching 4.6% in the process posting fresh 3-month highs.

- Following the US CPI stocks initially fell hard before recovering after one Fed rep said “In my view, we are not done yet…..but we’re nearing the point where rates were restrictive enough”.

- The composition of the print was also important, with shelter & energy big drivers, however, both of these aspects have seen easing since the data was collected, particularly shelter which makes up a whopping 25% of the CPI.

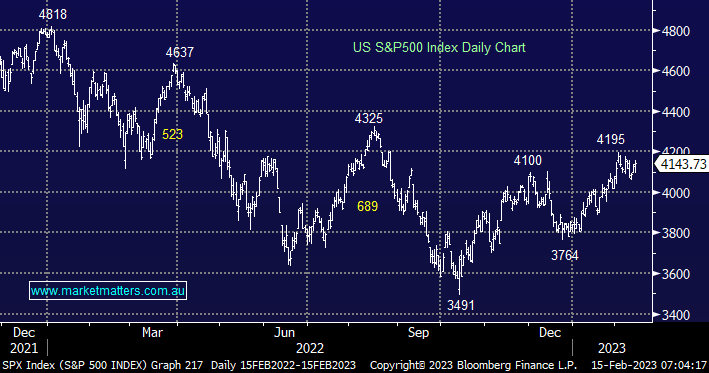

US indices rallied back after an initial dip after the CPI release e.g. the Dow initially fell over 400 points before recovering more than half of the knee-jerk losses to close down just 156 points but the standout was the tech-based NASDAQ which closed up +0.7% even as short-term bond yields marched higher.

- No change, our preferred scenario is the S&P500 will eventually see to a test of the 4300 area, or 4% higher.

MM remains cautiously optimistic about US stocks into Q1

Add To Hit List

US 2-year yields edged higher overnight but interestingly the $US fell and gold was unchanged suggesting this latest hawkish news on the inflation front was largely already priced into markets.

- We can see the US 2 years rotating in the 4 to 5% region over the coming months as investors 2nd guess the Fed through 2023/4.

MM is neutral to slightly bullish US short-term yields

Add To Hit List

Following an extremely strong January and early February, local stocks have moved into a consolidation phase as reporting season dominates the market. At MM our stance moving forward hasn’t changed at this early stage of the year:

- We will continue to adopt a buy weakness sell strength attitude through 2023 although more evenly balanced than in 2022 when we adopted a more bearish outlook.

- Stock and sector rotation will remain the key to adding value/alpha as inflation sentiment is likely to pivot at least once over the next 12 months i.e. we believe bond yields will dictate proceedings until further notice.