The ASX200 rallied strongly yesterday to close +1.1% on broad based buying and importantly an absence of meaningful selling – even the embattled Mining & Energy sectors reversed early loses to close marginally higher. However its was the tech names that finally performed the heavy lifting for the ASX with over 90% of the stock’s closing up on the day, assisting the sector post a healthy +3.3% gain. MM has been looking for the growth stocks to recover some of their recent declines, perhaps its will be a classic case of “sell the rumour & buy the fact” after the Feds interest rate decision this morning.

Yesterday’s strong advance was undoubtedly helped by the positive sentiment from Chinese stocks rallying the most since 2008 (GFC time!) following a vow out of Beijing to keep its stock market stable and support overseas listings – they must have taken a few weeks holiday in February & March! To put things into perspective heavyweights Alibaba (BABA US) and JD.com (JD US) both surged nearly 40% is US trading overnight – when we combine this with an outright +9% pop by the Hang Seng yesterday our solid +1.1% gain by the index felt pretty controlled, today will see some further catch up no doubt.

Nickel was at it again overnight, the exchange (LME) had to halt trading as the price plunged after a week-long suspension – what do they expect if they close a market for a week in today’s volatile environment! Most of the early morning trades were executed at $US45,590/tonne well under a half of last week’s panic high. Last weeks unprecedented short squeeze is clearly easing leaving MM comfortable waiting to see where the new equilibrium is reached.

The Fed raised interest rates 0.25% overnight as expected and importantly signalled 6 more hikes this year as they commenced a campaign to deal with the fastest inflation in over 40-yerars. Due to rates being at the artificially low 0.25% they actually doubled this morning to 0.5% but the most important point was the hawkish rhetoric which sent bond yields to their highest level in years, I truly hope mortgage holders are prepared for what’s coming because interest rates being “lower for longer” is a thing of the past.

Overnight we saw a choppy session where US stocks were strong early, fell back after the decision to hike rates, before rallying strongly into the close following Fed Chair Jerome Powell’s press conference, the Nasdaq leading the advance up nearly 4% – the SPI futures are pointing a very bullish open up around 1.5%.

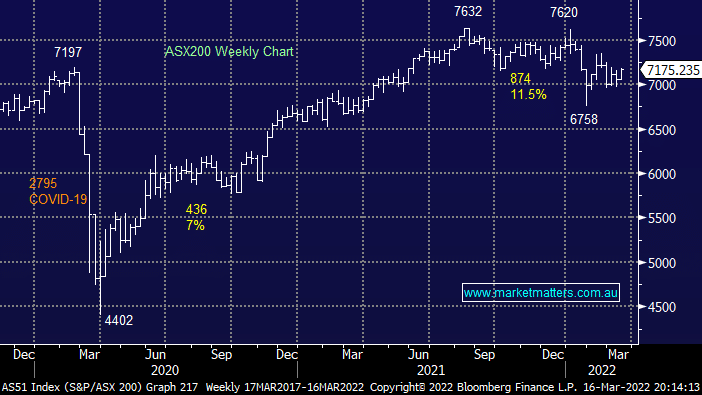

MM remains mildly bullish the ASX while its below 7200

Add To Hit List