The ASX200 rallied strongly yesterday to close +1.2% with exactly 80% of the market closing up on the day, the Financials were again the standout rallying +2.5% while the resources continued to look a touch tired although not down and out at this stage. Historically the banks simply love this time of year with 3 of the “Big Four” trading ex-dividend over the coming weeks however its this exact same seasonal strong rally by the sector which often bears fruit to the “sell in May & go away” trade for the ASX , to be precise just before the end of April is when the ASX usually gets the jitters – one for the back burner at this stage. We like our statistics at MM, obviously when we feel they have foundation, consider the below:

- Since the mid-1950’s equity markets have experienced 25 shocks from COVID to both the Iraq & Ukraine invasions.

- History tells us these “sell offs” surprisingly usually run out of steam in less than 3-weeks – the Russian invasion started on the 24th of February, only 2 ½ weeks ago.

- Following these 25 capitulations the market rallied 7.5% over the next month on over 85% of occasions – if nothing else it’s a dangerous time to be short / underweight.

Of course its easy to argue that statistics can be moulded to any argument but when we combine the above 3 points with the bullish seasonality around the ASX & banks we feel its hard to be too bearish local stocks over the next 4-6 weeks, a long time in today’s environment! Just for good measure we’ve recently seen major headwinds to “risk assets” from surging bond yields / inflation and the Ukraine invasion and subsequent supply shocks, its hard to imagine many more negative surprises weighing on the index, at least short-term.

NB All of the above ties in nicely with uncertainty creeping into the ASX as Mays likely election slowly gains traction.

Overnight we saw US stocks reverse early gains as volatility remained the constant, oil actually dipped back under $US100/barrel at one stage down over 8% which saw the Energy Sector down over 3.5%. Panic was the only word to describe the selling which smacked Chinese stocks yesterday as the index fell over 7% as the government continues to fight COVID with lockdowns – it doesn’t work guys! The futures market is now almost fully pricing in 7 US rate hikes of 0.25% this year as the hawks dominate, we think they may ultimately be slightly disappointed. The SPI futures are flagging the ASX to surrender ~70% of yesterday’s gains this morning not helped by BHP trading down $1.80 in the US.

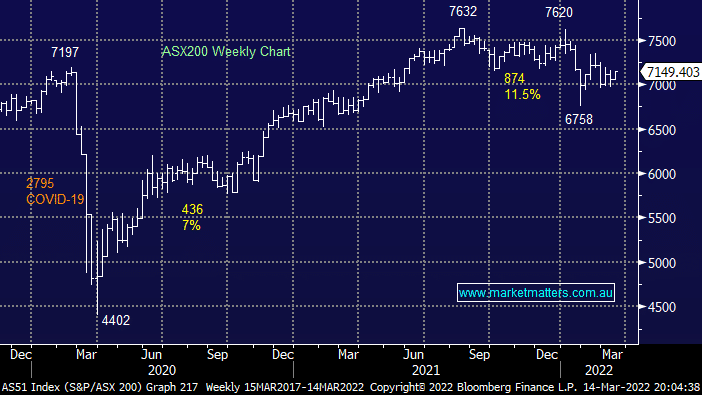

MM remains neutral to mildly bullish the ASX while its below 7200

Add To Hit List