Firstly, happy International Woman’s Day to all the wonderful female members of Market Matters, along with our sensational National Sales Manager Vanessa Chin, just back from maternity leave.

The ASX200 closed down 1% yesterday as the escalating Ukraine conflict continued to panic markets although we significantly outperformed other indices in the region due to our large resources exposure e.g. Japan, Hong Kong, India, and Korea all fell between 2% & 4%. We saw over 75% of stocks on the ASX200 decline on the day but when the influential energy and resource stocks rally strongly it undoubtedly helps shore up the local index.

As most subscribers will know the financial headlines were dominated by oil, and to a lesser extent gold, as investors flocked away from risk assets as the potential ban on Russian oil by Western consumers stoked crisis fears:

- Russia supplies around 7% of global oil hence we’ve witnessed Brent Crude prices soar over 58% during the 1st week of March alone, it feels overdone but that was our view late last week!

- Gold has already rallied over $US100/oz this March taking it above the psychological $US2,000/oz, another 3% and we’ll be at multi-decade highs.

On the macro bond yield front, it’s a battle/balance between inflation fears and concerns that soaring oil prices will choke the global economy, similar to how they did in the early 1970s. If history repeats itself investors should focus on the REITs and not surprisingly Gold & Energy stocks but it was a volatile journey which wasn’t for the fainthearted e.g. gold corrected 40% between 1974 & 1976 before exploding 800% over the following 4-years.

- MM reiterates our opinion that commodities have begun a “Super Cycle” but after an uninterrupted major rally since April 2020 we believe it’s time for a decent pullback i.e. the elastic band is stretching very taught

Overnight saw US stocks tumble over 2% led again by tech stocks but interestingly the SPI futures are calling the ASX to open unchanged following significant volume through the market, perhaps some fund managers are deploying part of the $35bn worth of dividends they will be receiving through March & April.

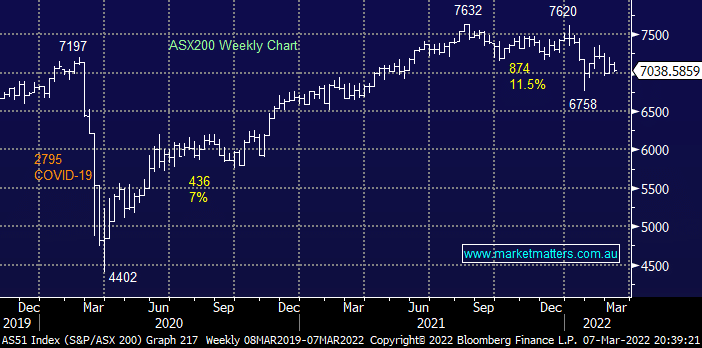

MM is neutral to bullish the ASX while it’s below 7200

Add To Hit List