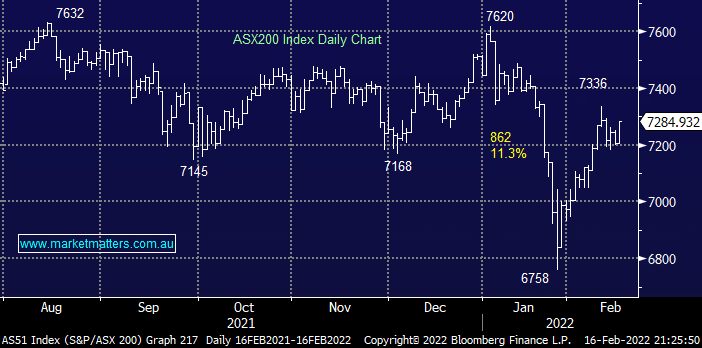

The ASX200 enjoyed a strong session on Wednesday although it was struggling into lunch as the “sell the strength” mentality that’s dominated most of 2022 took hold as S&P500 futures wobbled however solid broad based buying from 11am pushed the market higher and the index finally closed up more than 1% with 85% of stocks closing positive for the day. A few weeks ago we targeted some consolidation in the 7200 – 7400 region, in hindsight we underestimated how much it needed a rest and its been an even tighter range but still an encouraging platform for the bulls after Januarys painful start to the year.

There’s an old cliché in sport – it was a game of 2 halves and the markets relative performance yesterday was very much of that ilk:

Losers – Energy & Resources.

Winners – Everybody else spearheaded by the Healthcare & Real Estate Sectors.

We’ve clearly witnessed some sector rotation as the Ukraine concerns diminished however on the stock level we saw huge performance standouts with 17 stocks rallying by over 5%, and 4 over 10% while the iron ore, gold and energy stocks largely drifted lower. A number of companies that deliver a feel good factor rallied and we will focus on some of these later in today’s report along with the explanation of what we mean by the phrase.

Overnight US stocks closed largely unchanged after recovering from early losses following the Fed minutes which contain no nasty surprises – markets are positioned for the worst case scenario when it comes to rate hikes. The SPI futures are pointing to quiet start this morning which is encouraging following yesterdays strong gains.

MM remains bullish the ASX while its above 7200

Add To Hit List