Tuesday saw the ASX200 drift lower through the afternoon to finally close down 0.5%, again we saw more stocks in the losers corner but it was another sharp decline by iron ore, and its related miners, which overshadowed a recovery by the tech names. BHP Group (BHP) was the best of the bunch only slipping 0.3% after delivering a solid scorecard yesterday as it showcased the fruits of rising commodity prices for miners – if inflation & interest rates have bottomed we could indeed be in the early stages of a “Super cycle” for the Resources Sector.

- MM’s long term view is we have indeed entered a “Super Cycle” for commodities but we feel they are approaching a decent correction short / medium term.

I heard a quip from one of our team yesterday which made me laugh while it was on point, it went something like “all the COVID experts are now Ukraine specialists“ – well done Nitish! In our opinion the 2 main factors which will determine stock / sector and index performance through 2022 / 23 are straight from the old fashioned investors handbook:

- A company’s earnings, profitability and outlook moving forward will determine the stocks performance although as is always the case when human emotions (Fear & Greed) are involved there will be some “noise” along the way.

- Interest rates will determine share price valuations, we’ve recently seen a re-rating lower of the growth stocks in the anticipation of rapidly increasing interest rates i.e. if rates rise most stocks will fall all else being equal.

Obviously there are plenty of other moving parts when evaluating companies and the share market, not least being the health of the global economy, but at this stage we feel central banks wont hike rates too fast that they jeopardise growth but obviously it’s a balancing act that MM will be monitoring very carefully.

Overnight US stocks rallied strongly following comments that Putin was looking for a diplomatic solution while implementing a “partial” troop withdrawal. US stocks rallied strongly led by tech names, the S&P500 closed up 1.5% while the SPI Futures are calling the ASX200 to open up around 70-points with stock / sector moves likely to be magnified versions of yesterdays. Interestingly the overnight moves demonstrate that for now the Ukraine is more dominant on equity markets than inflation but that’s unlikely to last for long.

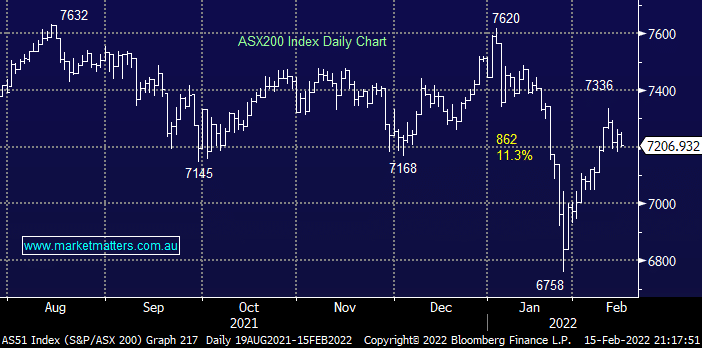

MM remains mildly bullish the ASX200 while it consolidates above 7200

Add To Hit List